Despite the BoC’s reality check, the crowd still believes lower interest rates are on the horizon.

As the Bank of Canada (BoC) upped the ante on Jun. 7, another rate hike materialized when the crowd assumed the race was over. Moreover, the central bank warned that more hawkish surprises could be on the horizon. The official press release read:

“Canada’s economy was stronger than expected in the first quarter of 2023, with GDP growth of 3.1%. Consumption growth was surprisingly strong and broad-based, even after accounting for the boost from population gains. Demand for services continued to rebound. In addition, spending on interest-sensitive goods increased and, more recently, housing market activity has picked up.

“The labour market remains tight: higher immigration and participation rates are expanding the supply of workers but new workers have been quickly hired, reflecting continued strong demand for labour. Overall, excess demand in the economy looks to be more persistent than anticipated.”

To that point, while we warned throughout 2022 that resilient demand would prove problematic, we noted on Apr. 6 that the theme would continue. We wrote:

While our prediction proved prescient as demand remained resilient throughout 2022 and inflation proved more problematic than expected, little has changed. Households’ checkable deposits have only declined slightly from their 2022 peak and are 362% above their Q4 2019 comparison.

Thus, when you combine this much cash with near-record-low unemployment and near-record-high wage inflation, investors are kidding themselves if they think demand destruction has arrived.

So, while our fundamental thesis continues to bear fruit, the PMs have corrected, but they remain relatively uplifted. As such, why is the selling pressure less persistent than in 2022? Well, it all comes down to expectations. With the crowd assuming the Fed will cut the U.S. federal funds rate (FFR) soon, there is little reason to fear higher interest rates when a new reality could emerge.

Please see below:

To explain, the gold line above tracks the GDXJ ETF, while the black line above tracks the iShares 20+ Year Treasury Bond (TLT) ETF. As you can see, the pair have largely moved in lockstep since late 2022. Furthermore, when long-term interest rates fall (black line rises), the PMs respond positively. And with the crowd so anxious for a recession to emerge, any hint of bad news causes them to bid long-term bonds.

Economic Resilience

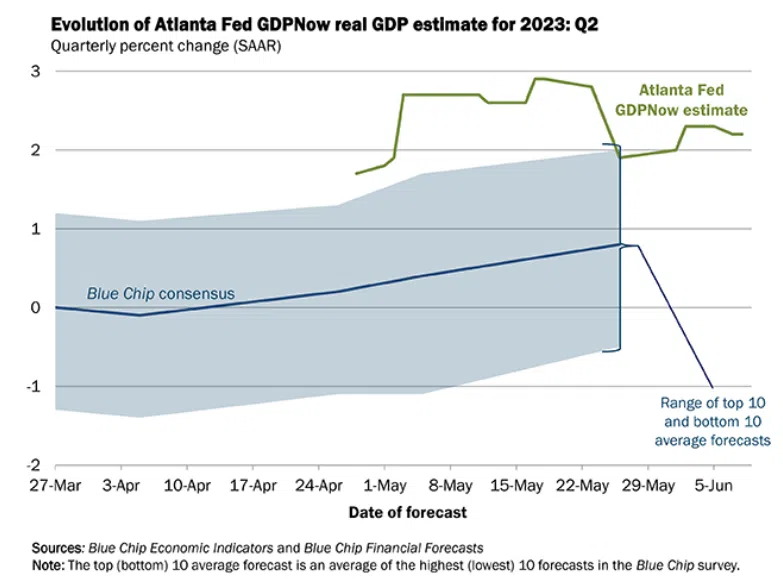

The Atlanta Fed updated its GDPNow forecast on Jun. 8. And with the metric standing at 2.2%, Q2 real GDP growth should remain uplifted and come in slightly above the pre-pandemic trend.

Please see below:

To explain, the green line above tracks the Atlanta Fed’s Q2 GDPNow estimate. As you can see, the data does not support investors’ economic pessimism.

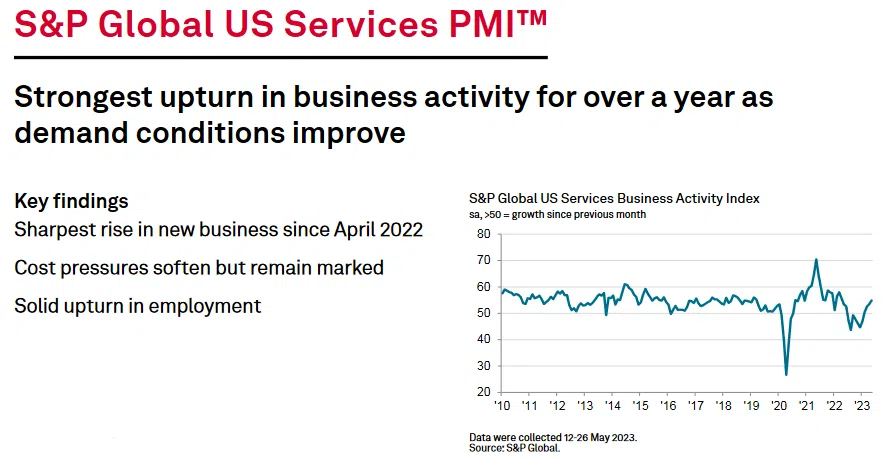

Likewise, S&P Global released its U.S. Services PMI on Jun. 5. And with the headline index increasing from 53.6 in April to 54.9 in May, solid demand dominated. The report stated:

“Contributing to the rise in new orders was a renewed upturn in new business from abroad in May. New export orders increased for the first time in a year, and at a solid pace. Demand conditions at new and existing customers reportedly strengthened to support the latest expansion.”

In addition:

“In line with a stronger expansion in new business, service sector firms increased their workforce numbers at a solid pace. Matching the payroll gain seen in April, the rate of job creation was the joint-fastest since August 2022.”

Thus, while we’ve warned on numerous occasions that interest rates are too low to create the demand destruction necessary to eradicate inflation, the crowd continues to price in a pivot. However, we expect a profound wake-up call to emerge over the medium term.

Please see below:

Finally, with resilient demand uplifting employment, the Atlanta Fed’s Wage Growth Tracker came in at 6% on Jun. 8, which is only 0.1% below the April figure. Therefore, with sticky salaries poised to keep consumer spending and output inflation sturdy, interest rates should seek higher ground before it’s all said and done.

Overall, while the crowd believes that bond prices will trend higher, the fundamentals do not support their assertion. Economic activity has not cratered, and the bond bulls help the PMs by pricing in a recession that has not materialized. In reality, when long-term interest rates fall, they stimulate growth by making financing more affordable. So, it’s no wonder the BoC noted how “spending on interest-sensitive goods increased and, more recently, housing market activity has picked up.”

Consequently, while the consensus expects less, we believe the Fed will have to do more to win this inflation war.

Do you believe the Fed and BoC will keep hiking?

Alex Demolitor

Precious Metals Strategist