Should gold read between the lines or follow the pivot narrative?

With investors anticipating Fed Chairman Jerome Powell’s speech on Jan. 10, anxiety was amplified ahead of the typically market-moving event. However, with the central bank chief not commenting directly on the future path of interest rates, the event didn’t live up to the hype.

Yet, with not-so-subtle clues signaling what’s to come, Powell said:

“Price stability is the bedrock of a healthy economy and provides the public with immeasurable benefits over time. But restoring price stability when inflation is high can require measures that are not popular in the short term as we raise interest rates to slow the economy.

“The absence of direct political control over our decisions allows us to take these necessary measures without considering short-term political factors.”

So, while Powell stated that controlling inflation requires “measures that are not popular in the short term,” he reiterated his belief that a steady rise in the U.S. federal funds rate (FFR) is preferable to a stop-go approach.

Furthermore, his mention of “short-term political factors” was a direct pushback against the Democrats, who falsely assume that a dovish pivot will keep the unemployment rate from rising. In reality, letting unanchored inflation run often results in worse recessions than accepting the consequences of a higher FFR.

Likewise, while the crowd has ignored Fed officials’ hawkish warnings in recent weeks, Powell largely confirmed their message on Jan. 10. As a result, higher interest rates and continued QT should remain prevalent in the months ahead.

To that point, Fed Governor Michelle Bowman said on Jan. 10:

“It’s important to keep in mind that there are costs and risks to tightening policy to lower inflation, but I see the costs and risks of allowing inflation to persist as far greater….

“I expect that once we achieve a sufficiently restrictive federal funds rate, it will need to remain at that level for some time in order to restore price stability, which will in turn help to create conditions that support a sustainably strong labor market.”

Thus, it was another day, and another dose of reality that the financial markets ignored.

Please see below:

Source: Bloomberg

Source: Bloomberg

On top of that, the NFIB released its Small Business Optimism Index on Jan. 10; and while the net percentage of firms increasing their output prices declined in December, the report stated:

“A net 44 percent reported raising compensation, up 4 points from November. A net 27 percent plan to raise compensation in the next three months, down 1 point from November.”

Consequently, while we warned that wage inflation would remain a thorn in the Fed’s side, the uptick in December highlights the challenges that lie ahead.

Please see below:

Source: NFIB

Source: NFIB

To explain, the net percentage of firms reporting actual compensation changes (the black line above) re-accelerated in December, and remains elevated relative to its historical norm. In addition, while the gray line above signals that fewer small businesses expect higher wages in the months ahead, the divergence emphasizes the realities on the ground: while firms may want to reduce their employment costs, the supply/demand imbalance in the U.S labor market is not helping.

As a result, it’s unrealistic for the Fed to materially reduce output inflation when wages are running at 6%+.

As further evidence, the NFIB summary read:

Source: NFIB

Source: NFIB

So, while investors celebrate the reduction in oil prices and their impact on the headline Consumer Price Index (CPI), the NFIB highlighted how “cutting selling prices is easy” when “the cost of inputs like fuel or inventory fall.”

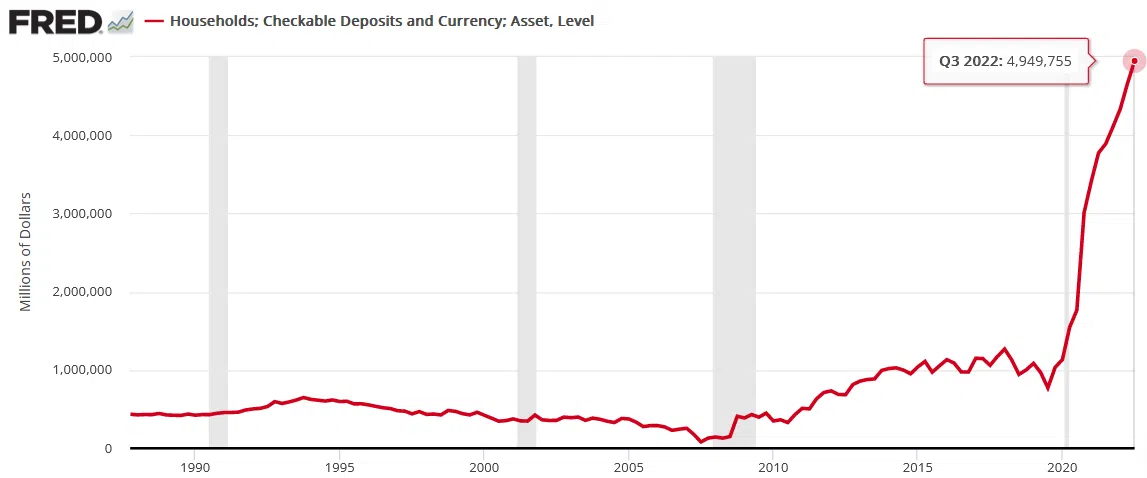

In contrast, wages are much more problematic, and with the growth occurring alongside record household checkable deposits, the impacts of unprecedented stimulus are far from resolved. To explain, we wrote on Dec. 13:

While the FFR has surged in 2022 and the crowd still assumes that demand will collapse, the Fed revealed on Dec. 9 that U.S. households have a record ~$4.95 trillion (as of Q3 2022) in their checking and/or demand deposit accounts, which is 379% more than Q4 2019 and 6.3% more than Q2 2022.

Please see below:

Consequently, while investors wait for a destitute consumer to reduce inflation and allow the Fed to pivot, the vertical ascent on the right side of the chart above highlights the profound stimulus imbalance that materialized during the pandemic; and with wage growth also near an all-time high, investors are kidding themselves if they think monetary policy can return to its pre-pandemic state when Americans’ checking account balances have gone parabolic.

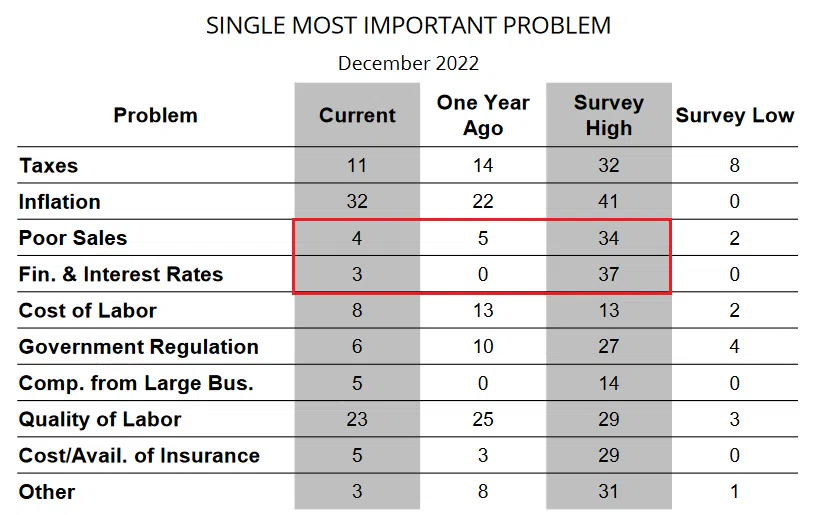

Continuing the theme, the NFIB revealed that interest rates and poor sales are among the least pressing issues confronting U.S. small businesses.

Please see below:

Source: NFIB

Source: NFIB

To explain, the table above tracks the net percentage of firms that cite a particular issue as their “single most important problem.” If you analyze the red rectangle, you can see that poor sales declined from 5 in December 2021 to 4 in December 2022. Furthermore, with the current metric nowhere near the survey high of 34, demand destruction is not small businesses’ primary concern.

Likewise, while the FFR soared in 2022, the net percentage of firms lamenting higher interest rates only increased from 0 in December 2021 to 3 in December 2022, which is far from the survey high of 37.

Therefore, small businesses are most concerned about inflation, while worries about higher interest rates and demand destruction are nowhere near crisis levels.

As such, while the crowd assumes that a lower headline CPI means the Fed is near a pivot, the resiliency of core inflation highlights the embedded pricing pressures. Moreover, even though the headline CPI decelerated in November, the Atlanta Fed’s headline and core Sticky CPIs hit new 2022 highs. As a result, asset prices do not reflect the hawkish realities that should confront the financial markets in the months ahead.

Overall, gold has begun the New Year on a high note, as stock, bond and currency markets seem inclined to buy the pivot narrative. Yet, the fundamentals don’t support their conclusion, and dovish re-pricings throughout 2022 ended badly for the bulls. Consequently, we see this iteration as no different.

Let us know what you think. Why is the crowd so dismissive of the hawkish ramifications? Or, is the consensus right to expect a dovish pivot? How does gold respond if this week’s CPI print comes in cooler than expected?

Alex Demolitor

Precious Metals Strategist