Ominous signs are forming across the precious metals market.

While gold ended the day roughly flat on Jan. 27, mining stocks were major laggards, despite the S&P 500’s rally. In addition, with silver unable to hold $24 and the USD Index showing signs of forming a bottom, a reversal of fortunes could be on the horizon.

For example, Danske Bank analysts wrote on Jan. 27:

“To the extent central banks next week (primarily Fed, ECB) deliver a fairly firm hawkish guidance – especially when taking into account the last quarter's easing of financial conditions – we think a long USD position is beginning to look appealing again, perhaps even from a tactical perspective. Either way next week could prove pivotal for the global investment environment that will face us for the rest of February.”

They added:

“As explained over the last weeks, we still have a strategic bearish bias for the EUR/USD even if our tactical conviction is less clear.”

For context, “strategic” means over the medium term, while “tactical” means over the short term.

Thus, this week is riddled with market-moving events and volatility could be amplified. We have the Fed and ECB monetary policy meetings. There are also PMIs, nonfarm payrolls, and earnings from heavyweights like Apple, Amazon and Alphabet. As a result, the cross-asset implications could be material.

Despite that, the USD Index has demonstrated relative strength in recent days, and its inability to decline amid the ‘soft landing’ momentum and economic data speaks volumes. Furthermore, with looser financial conditions only spurring more inflation, Fed Chairman Jerome Powell needs to push back against these developments to avoid exacerbating the problem.

Please see below:

To explain, the red line above tracks the U.S. federal funds rate (FFR), while the blue line above tracks the Goldman Sachs Financial Conditions Index (FCI). If you analyze the movement of the blue line, you can see that financial conditions have eased materially in recent months, which helped uplift the PMs.

Conversely, the blue line’s peak in September and October occurred alongside the 2022 lows for gold, silver and mining stocks; and with a higher FCI needed to curb inflation, a dovish Powell would only worsen the situation. Therefore, it’s in his best interest to reverse this trend, and a realization is bullish for the USD Index and real yields, and bearish for the PMs.

To that point, we noted on Jan. 5 that the FOMC’s latest monetary policy minutes emphasized the pitfalls of easier financial conditions.

Please see below:

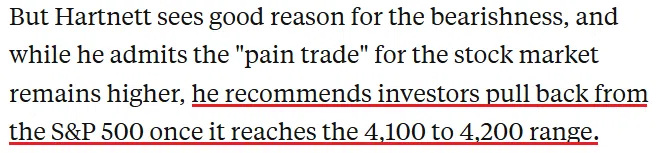

Likewise, with signs of reversals becoming more prevalent, Bank of America’s Chief Investment Strategist Michael Hartnett sees a narrative shift forthcoming in the days and weeks ahead. He wrote on Jan. 27:

“All signals [suggest a] hard landing will occur in 2023; but another tightening of financial conditions this spring may be required to tip a U.S. economy currently growing >7% in nominal terms into the recession the consensus craves.”

So, with Bank of America expecting that a re-acceleration in inflation will reverse investors’ rate-cut expectations, he told clients that the S&P 500 should be sold in the 4,100 to 4,200 range as the next leg lower is near. For context, the S&P 500 hit an intraday high of 4,094 on Jan. 27.

Please see below:

On top of that, while lower energy prices have helped reduce headline inflation recently, the deceleration has led to an increase in Americans' real (inflation-adjusted) incomes. Although, we warned throughout this cycle that demand was the primary driver of inflation, and higher real incomes are bullish for consumption.

Please see below:

To explain, the red and blue lines above track the three and six-month percentage changes in real personal income minus transfer payments (government benefits). If you analyze the right side of the chart, you can see that the metrics have been rising for the last six months and are up by an annualized rate of 2.9%. Thus, while the pivot crowd proclaims that a destitute consumer will allow for a dovish 180, the realities of near-record-high wage inflation tell a different story.

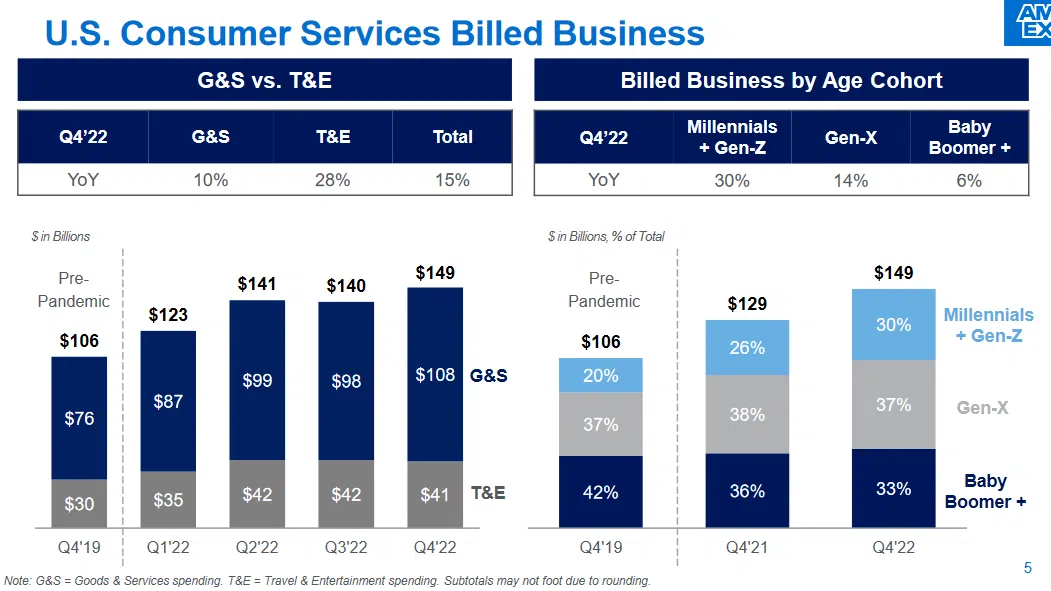

Speaking of which, American Express – one of the largest U.S. credit card issuers – released its fourth-quarter earnings on Jan. 27. CFO Jeff Campbell said during the Q4 conference call:

“Starting with our largest segment, U.S. consumer billings grew 15% in the fourth quarter, reflecting the continued strength and spending trends from our premium U.S. consumers. Our focus on attracting, engaging, and retaining younger cohorts of cardmembers to our value propositions drove the 30% growth in spending from our millennial and Gen Z customers.”

He added:

“Across all customer types, T&E spending momentum remained particularly strong in the fourth quarter, while we also saw a nice sequential growth in the amount of goods and services spending versus last quarter.”

Please see below:

To explain, the figures at the top left of the chart above show that consumers’ goods & services (G&S) spending increased by 10% year-over-year (YoY) in Q4, while travel & entertainment (T&E) was up by 28%. In addition, the figures at the top right show that spending was also resilient across different age groups. As a result, the fundamentals continue to unfold as expected, and the crowd underestimates how high the FFR needs to rise to suppress demand and normalize inflation.

For context, we wrote on Mar. 31, 2022:

We’ve noted for some time that the U.S. economy remains in a healthy position; and with U.S. consumers flush with cash and a red hot labor market helping to bloat their wallets, their propensity to spend keeps economic data elevated. Likewise, while most investors assumed that consumer spending and inflation would fall off a cliff when enhanced unemployment benefits ended in September, the reality is that neither will die easy.

Overall, the PMs have begun to showcase relative weakness, as their rallies have sputtered despite a higher S&P 500. Moreover, while gold has been somewhat calm, silver’s volatility and mining stocks’ recent lull are ominous signs of what’s likely to come. So, while headline risk is amplified this week, the medium-term implications are unchanged.

How will Powell react to the FCI’s recent pullback? Will Hartnett be right about the S&P 500’s medium-term peak? Why is consumer spending so resilient? Please share your thoughts.

Alex Demolitor

Precious Metals Strategist