A USD Index reversal could upend the gold price.

Despite rallying sharply intraday on Feb. 2, gold reversed its gains and closed lower, while the USD Index reversed its losses and closed higher. As a result, while the recent gambit of ‘dollar down, gold up’ has helped uplift the PMs, a reversal of fortunes could be on the horizon.

Furthermore, while the crowd assumes that inflation will decline smoothly to 2%, its propensity to jump around should collapse this narrative and enhance volatility. Again, it’s not that inflation will hit new highs; it’s that it won’t return to 2% without immense demand destruction; and since that demand destruction is not present now, interest rates need to rise to suppress consumption and rebalance the U.S. labor market.

To that point, while supply-chain disruptions are a thing of the past, S&P 500 companies still maintain pricing power, which highlights the resiliency of demand; and with corporations poised to continue their hiking spree until demand dissipates, the medium-term outlooks are bullish for the U.S. federal funds rate (FFR), the USD Index, and real yields.

For example, even Waste Management – North America’s largest recycling and garbage collector – plans to raise its fees in 2023. COO John Morris said during the Q4 conference call on Feb. 1:

“As we move into 2023, our disciplined pricing programs combined with the strong momentum from 2022 and are expected to deliver core price of between 6.5% and 7% with yield approaching 5.5%. Our expectation is for strong rollover of 2022 price performance.”

Likewise, Mondelez – one of the largest confectionary companies in the U.S. – released its fourth-quarter earnings on Jan. 31; and with pricing the main driver of its performance, it’s naïve to assume that the Consumer Price Index (CPI) will return to 2% when major corporations are still posting higher figures.

Please see below:

To explain, the blue box above shows that Mondelez recorded 19.5% year-over-year (YoY) organic revenue growth in North America in Q4. For context, the metric excludes the impact of acquisitions, divestitures and currency fluctuations. More importantly, the red box above shows that a 15.3% YoY increase in pricing was the main driver of the top-line strength. Consequently, the realities on the ground contrast with the narrative on Wall Street.

To that point, Mondelez CFO Luca Zaramella said during the Q4 conference call:

“As far as assumptions grow, we are planning for another year of double-digit inflation with dollars higher than in 2022. This inflation is driven by the continued elevated cost in packaging, energy, ingredients and labor.”

So, while we’ve warned repeatedly that corporations will continue to increase their prices until their costs normalize (which requires higher interest rates to suppress demand), Mondelez expects 2023 to look a lot like 2022.

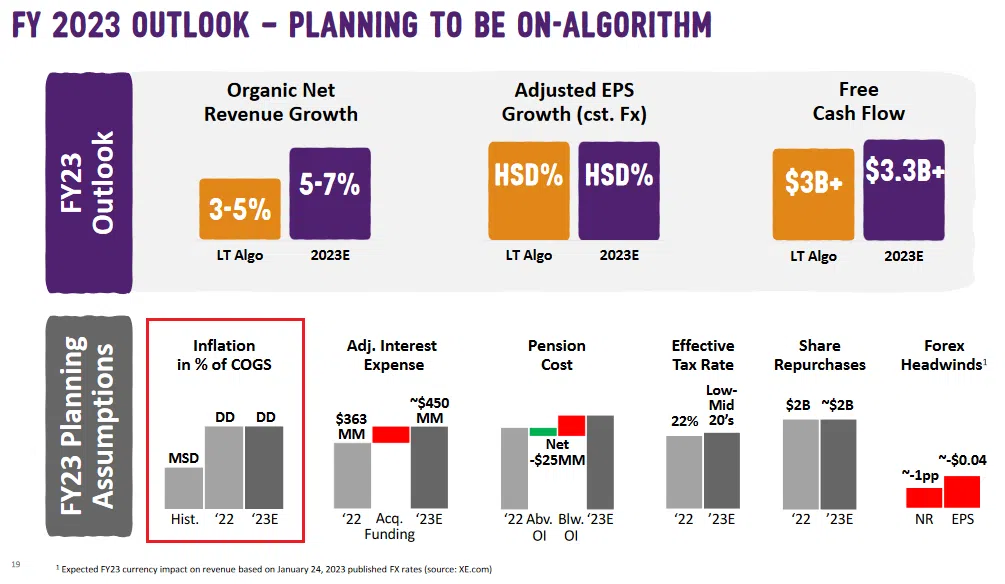

Please see below:

To explain, the red box above shows that Mondelez expects its 2023 inflation as a percentage of its cost of goods sold (COGS) to match 2022. More importantly, notice how the realized 2022 and estimated 2023 figures are roughly double their historical norm (labeled Hist.)?

Again, it’s not that we expect the CPI to run to 10%, but investors are kidding themselves if they think it will return to 2% when real economy companies are raising their prices by much more.

As further evidence, Hershey – another confectionary giant – released its fourth-quarter earnings on Feb. 2; and like Mondelez, the company also increased its prices materially.

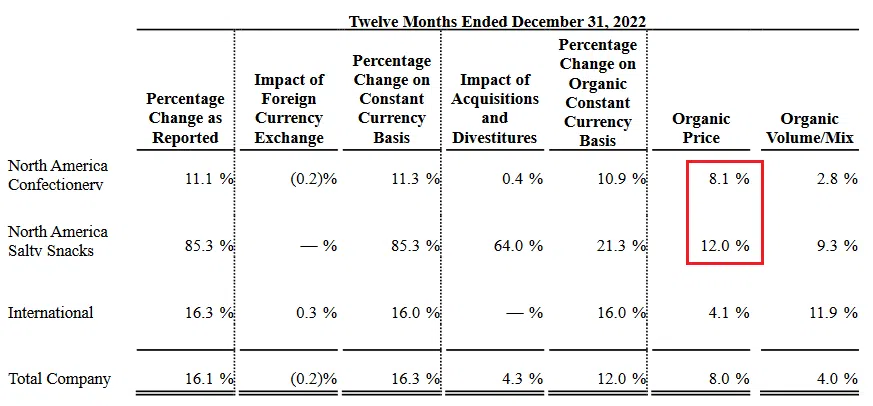

Please see below:

To explain, organic price increases across North America Confectionary and Salty Snacks were 8.1% YoY and 12% YoY, respectively, in Q4. Therefore, like the Sticky CPIs imply, inflation is much more prevalent than the narrative proclaims.

Furthermore, to normalize inflation, demand needs to decline to the point where companies stop raising prices; and as that occurs, they will reduce their headcount, which further decreases demand as the unemployment rate rises and consumers have less money to spend. But, the labor market remains resilient.

Please see below:

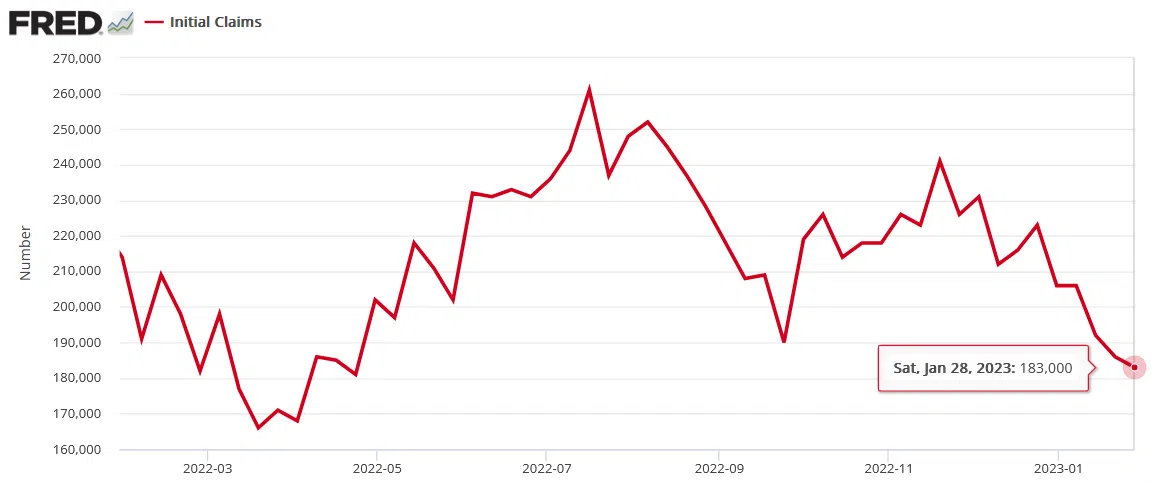

To explain, initial and continuing jobless claims outperformed expectations on Feb. 2; and the performance of the former highlights why the Fed has not done enough.

Please see below:

To explain, initial jobless claims track the number of Americans applying for unemployment benefits for the first time. If you analyze the movement, you can see that initial claims have been in a downtrend since mid-July, demonstrating how the Fed’s 18 rate hikes (25 basis point increments) have not collapsed the U.S. labor market.

The important point is that without rising unemployment, the persistent supply/demand imbalance is bullish for wage inflation, the FFR, real yields and the USD Index.

Finally, Challenger, Gray & Chirstmas Inc. released its job cuts report on Feb. 2. An excerpt read:

“U.S.-based employers announced 102,943 cuts in January, a 136% increase from the 43,651 cuts announced in December. It is 440% higher than the 19,064 cuts announced in the same month in 2022.”

However:

“The Technology sector announced the most cuts with 41,829, 41% of all cuts announced in January…. Since November 2022, which saw the highest monthly total for the sector since Challenger began tracking in 1993 with 52,771, Technology companies have announced 110,793 job cuts. January’s total is the second-highest for the sector on record.”

As a result, with the work-from-home bubble deflating, technology companies that over-hired during the pandemic are now slashing their headcount. Thus, it skews the consolidated metric upward and makes the headline number look worse. In other words, industries outside technology and real estate (pandemic and QE beneficiaries) remain resilient.

Please see below:

Overall, the fundamentals continue to unfold as expected, and the crowd underestimates the resiliency of inflation. Moreover, with nine of the last 10 bouts of rising inflation ending with recessions, it’s likely a matter of when, not if, the next rendition occurs; and with the USD Index showcasing immense resiliency in recent days despite the misguided narratives, the days of ‘USD Index up, PMs down’ should return sooner rather than later.

How likely is a USD Index comeback over the next few months? Will a resilient labor market push the FFR higher, or will demand collapse and allow the Fed to pivot? What do you make of the inflation results from the recent earnings reports?

Alex Demolitor

Precious Metals Strategist