QT and rate hikes should shift the narrative in 2023.

With risk assets looking to end 2022 on a high note, gold, silver, mining stocks and the S&P 500 rallied on Dec. 23. However, with sentiment shifting after each economic release, the recent results support a higher U.S. federal funds rate (FFR) in 2023.

For example, the Atlanta Fed updated its fourth-quarter real GDP growth estimate on Dec. 23; and with the projection remaining resilient, more hawkish policy should commence in the months ahead. The report stated:

“The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2022 is 3.7 percent on December 23, up from 2.7 percent on December 20…. The nowcasts of fourth-quarter real personal consumption expenditures growth and fourth-quarter real gross private domestic investment growth increased from 3.4 percent and -0.2 percent, respectively, to 3.6 percent and 3.8 percent, respectively.”

Please see below:

To explain, the green line above tracks the Atlanta Fed’s Q4 real GDP growth estimate, while the blue line above tracks the Blue Chip consensus estimate (investment banks). If you analyze the right side of the chart, you can see that the green line remains relatively elevated, given that U.S. real GDP growth tracked near 2% pre-pandemic.

As a result, with inflation highly problematic and economic growth far from crisis levels, the FFR should continue its ascent and accelerate the liquidity drain.

To that point, while inflation slowed in November due to the decline in asset prices that occurred in September/October, the Personal Consumption Expenditures (PCE) Index met expectations on Dec. 23.

But, while the crowd views the development as bullish, they miss the forest through the trees. We warned on numerous occasions that rampant wage inflation is the hawkish canary in the coal mine. In a nutshell: wage inflation drives output inflation because Americans can afford price increases that match their salary increases.

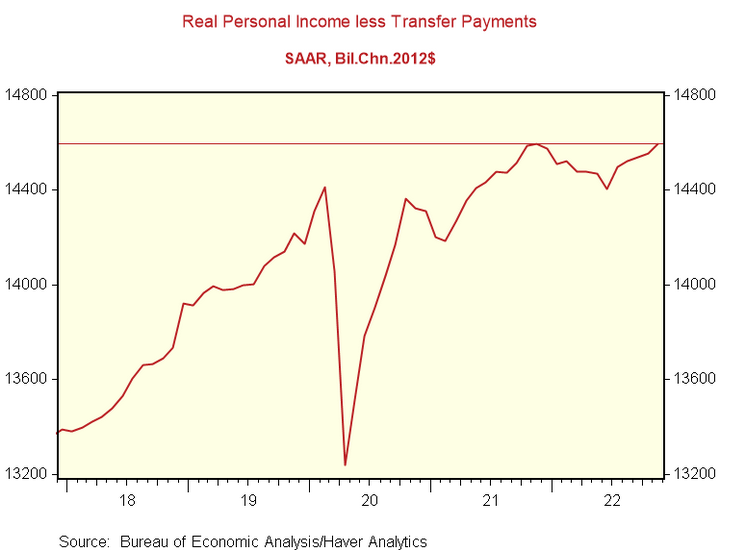

Yet, with wage inflation re-accelerating in November, while asset prices declined in September/October, it created the perfect backdrop for a rise in real (inflation-adjusted) incomes.

Please see below:

To explain, the red line above tracks consolidated real income minus transfer payments (government benefits). For context, the metric measures the change in Americans’ inflation-adjusted incomes after removing the impact of social security benefits, state pensions, unemployment benefits, etc.

If you analyze the right side of the chart, you can see that the red line has risen in recent months and has been running at an annualized rate of 3.2% since June.

So, with wage inflation outperforming output inflation recently, Americans’ real spending power has increased, which supports more discretionary purchases in the months ahead. Thus, the fundamentals are bullish for the FFR, real yields and the USD Index, and the crowd underestimates the resiliency of demand.

Speaking of which, Mastercard released its SpendingPulse U.S. retail sales report on Dec. 9. An excerpt read:

“U.S. retail sales excluding automotive were up +8.1% year-over-year (YoY) in November. E-commerce sales were up +5.9% YoY while in-store sales were up +8.6% YoY.”

As such, while consumer spending remains robust relative to its pre-pandemic level (the right column), it’s also highly resilient versus November 2021 (the left column). Therefore, the economic pain that spurs dovish pivots is largely non-existent.

Please see below:

To that point, while the FOMC reiterated its hawkish commitment on Dec. 14, the Bank of Canada (BoC) decided to adopt a wait-and-see approach. Although, we warned on Dec. 8 that the fundamentals do not support a pause anytime soon. We wrote:

While the BoC cited “excess demand” and “unemployment near historic lows,” and in the next breath, questioned “whether the policy interest rate needs to rise further,” the contradiction highlights the conundrum confronting North American central banks. With some areas of their economies running too hot, while others are too cold, they want to have their cake and eat it too.

However, the reality is that supporting growth encourages inflation, and history shows the gambit ends in a recession regardless of what they do; and while the BoC (and maybe the Fed next week) thinks the overnight lending rate could peak at 4.25%, we believe the central bank materially underestimates the challenges that lie ahead.

Likewise, with the recent data coming in hotter than expected, this Bloomberg headline from Dec. 23 is another example of the crowd's fallibility; and while the consensus peak FFR (and Canada's overnight lending rate) expectation has risen from 3% to 5% (4.25% in Canada), demand destruction has not materialized to the extent required to reduce inflation.

Please see below:

Source: Bloomberg

Source: Bloomberg

Finally, while the PMs have ignored the development, the U.S. 10-Year real yield has been on fire in December. After completing its consolidation and hitting a countertrend low of 1.08% on Dec. 2, the metric has soared by 47 basis points and ended the Dec. 23 session at 1.55%. Furthermore, it’s only 19 basis points away from its 2022 high of 1.74%, so gold is ignoring the ominous development at its own peril.

Overall, bullish seasonality has investors prioritizing sentiment, while history shows that normalizing unanchored inflation results in profound economic pain. Moreover, the crowd assumes that interest rates have peaked, corporate profits will stay elevated and inflation will magically disappear with little help from the other two (higher interest rates and lower corporate profits). But, their expectations contrast history and fundamental logic, and a profound wake-up call should occur in 2023.

Alex Demolitor

Precious Metals Strategist