The Russia-Ukraine crisis can provide valuable lessons.

With China ending its zero-COVID policy on Dec. 26, the bulls rejoiced as the second-largest importer should uplift economically-sensitive commodities; and with the optimism spreading to the precious metals, gold, silver and mining stocks joined in the festivities. However, while immaterial catalysts help push the PMs higher, the domestic fundamentals continue to deteriorate.

For example, we’ve noted how the U.S. 10-Year real yield has risen rapidly in December; and after ending the Dec. 27 session at 1.58%, the metric has rallied by 50 basis points from its Dec. 2 low, and is only 16 basis points below its 2022 high.

Furthermore, with nominal interest rates seeking higher ground as well, ignoring the developments came back to haunt the bulls in 2021 and 2022.

Please see below:

To explain, the gold line above tracks the gold futures price, while the red line above tracks the iShares 20+ Year Treasury Bond (TLT) ETF. For context, bond prices move inversely to interest rates, so the TLT ETF declines when long-term interest rates rise.

If you analyze the relationship, you can see that the pair had largely moved in lockstep in the years before the pandemic. Yet, with misguided investors assuming that new rules apply post-pandemic, the yellow metal has outperformed the TLT ETF.

Conversely, the divergences on the right side of the chart highlight how gold declined sharply when it attempted to run away from the TLT ETF. In mid-2021, the red line declined materially as long-term interest rates rose and gold headed in the opposite direction. Soon after, though, gold suffered a sharp drawdown and gave back most of its gains.

Likewise, when the Russia-Ukraine crisis sent gold soaring in February/March 2022, the TLT ETF was already in the midst of its monumental decline; and surprise, surprise, the gold price fell hard and sunk to new lows.

So, with the red line declining on the right side of the chart, the TLT ETF has given back roughly half of its countertrend rally. Conversely, gold continues to rise, and another divergence has materialized.

Thus, with a third rendition unfolding now, we expect the gold price to fall sharply in the months ahead. Remember, the Fed needs higher long-term interest rates to cool inflation, and the recent economic data has been hawkish, not dovish. That’s why the TLT ETF is down by 8.5% from its December closing high.

On top of that, the global liquidity drain continues to accelerate, as the Fed, the ECB, and even the BOJ have upped the hawkish ante. As such, while stocks and bonds got the bearish memo in February/March 2022, the PMs were the last to suffer; and with stocks and bonds selling off in December, the PMs are ignoring the developments at their own peril. Consequently, gold’s medium-term outlook remains highly bearish.

From another angle, while the GDXJ ETF’s rally has been more pronounced relative to gold, its medium-term plight has almost mirrored the TLT ETF. Therefore, its likely reversal should be even sharper.

Please see below:

To explain, the gold line above tracks the GDXJ ETF, while the red line above tracks the TLT ETF. If you analyze the relationship, you can see that the GDXJ ETF has been more volatile than gold, and it’s also declined by more from its post-pandemic high.

In addition, with a similar divergence on the right side of the chart, the TLT ETF’s recent rout highlights why the PMs’ uprisings are unsustainable. Not only are non-yielding assets less attractive when interest rates rise, but we saw this movie throughout 2021 and 2022: when momentum investors decouple the PMs from long-term nominal and real yields, sharp drawdowns unfold when they rush for the exits.

Please remember that momentum investors don’t care about the fundamentals. As long as their algorithms are flashing green, they ride the hot hand until sentiment shifts. However, the gambit is risky because waterfall declines often occur when everyone tries to exit at once, and the next bout of panic should be no different.

On top of that, while we warned throughout 2021 and 2022 that interest rates would rise from the ashes, the fundamentals still support a higher U.S. federal funds rate (FFR) in 2023. For context, while the consensus has predicted demand destruction for many months, we warned that American households are still flush with cash. We wrote on Dec. 13:

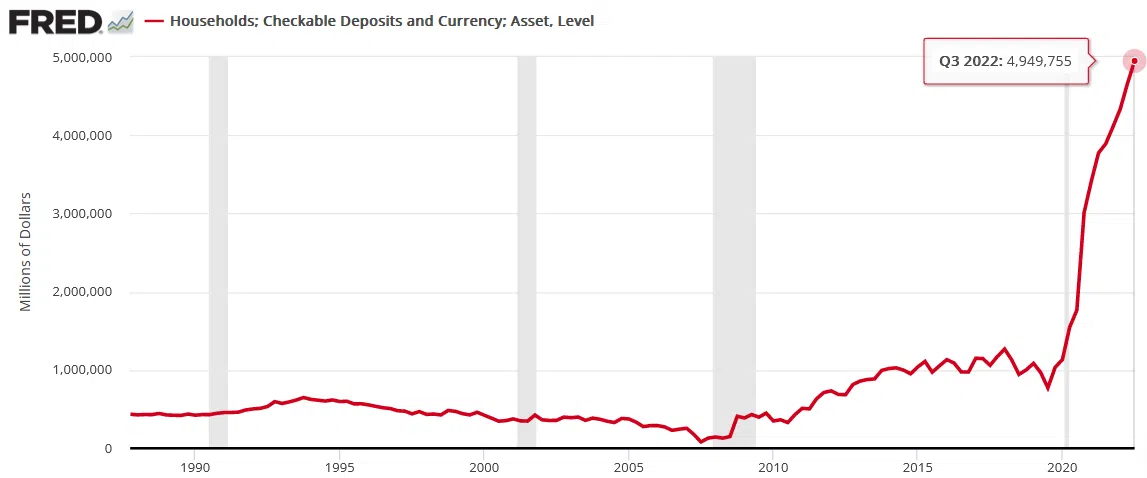

While the FFR has surged in 2022 and the crowd still assumes that demand will collapse, the Fed revealed on Dec. 9 that U.S. households have a record ~$4.95 trillion (as of Q3 2022) in their checking and/or demand deposit accounts, which is 379% more than Q4 2019 and 6.3% more than Q2 2022.

Please see below:

While investors wait for a destitute consumer to reduce inflation and allow the Fed to pivot, the vertical ascent on the right side of the chart above highlights the profound stimulus imbalance that materialized during the pandemic; and with wage growth also near an all-time high, investors are kidding themselves if they think monetary policy can return to its pre-pandemic state when Americans’ checking account balances have gone parabolic.

To that point, Mastercard revealed on Dec. 26 that holiday retail sales remained buoyant. The report stated:

“U.S. retail sales excluding automotive increased 7.6% year-over-year (YoY) this holiday season, running from November 1 through December 24…. Online sales grew 10.6% compared to the same period last year,” while “in-person dining continued to show strong momentum with restaurants up 15.1% YoY.”

Michelle Meyer, North America Chief Economist at the Mastercard Economics Institute, said:

“Inflation altered the way U.S. consumers approached their holiday shopping – from hunting for the best deals to making trade-offs that stretched gift-giving budgets. Consumers and retailers navigated the season well, displaying resilience amid increasing economic pressures.”

Please see below:

Overall, the fundamentals continue to unfold as expected: U.S. consumers remain resilient, and their ability and willingness to spend should keep the economic data elevated and put upward pressure on interest rates. As a result, with nominal and real yields on the rise in December, it’s likely only a matter of time before the PMs follow stocks and bonds lower.

Alex Demolitor

Precious Metals Strategist