Will the Fed Chairman get his soft landing?

While the day began gloomy as interest rate uncertainty reigned, Fed Chairman Jerome Powell’s press conference helped spur risk appetite. Moreover, with the crowd pricing in more rate cuts in the months ahead, they can almost smell the return of pre-pandemic monetary policy. However, while sentiment has shifted, little has changed fundamentally.

For example, the FOMC statement read:

“The Committee decided to raise the target range for the federal funds rate to 4-1/2 to 4-3/4 percent. The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”

Thus, while the FOMC braces for “ongoing increases,” the crowd expects ‘ongoing decreases.’ Furthermore, while Powell flip-flopped from hawkish to dovish throughout his press conference, he said, “Given our outlook, I don’t see us cutting rates this year.”

“We’ve raised rates four and a half percentage points, and we’re talking about a couple of more rate hikes to get to that level we think is appropriately restrictive. Why do we think that’s probably necessary? We think because inflation is still running very hot.”

Conversely, he added:

“We can now say I think for the first time that the disinflationary process has started. We can see that and we see it really in goods prices so far.”

Then, he said:

As a result, Powell was all over the place on Feb. 1, and his indecisive comments were perceived as bullish. In other words, since Powell didn’t spoil the party, why leave?

But, there seems to be a misperception that Powell can control the fundamentals. In a nutshell: his words are meaningless regarding their ability to control the business cycle. Yes, his rhetoric shifts sentiment and moves markets in the short term, but it’s largely irrelevant over the medium term.

Please see below:

To explain, the Bloomberg headline above was from Aug. 27, 2021. Back then, Powell and the bulls assumed that QE would continue for months and that rate hikes wouldn’t commence until 2023. Yet, those projections were way off, and the FOMC has raised interest rates 18 times in 2022 (25 basis point increments).

As it stands, this was the most important quote of Powell’s Feb. 1 press conference:

And therein lies the debate. Powell ‘thinks’ the U.S. will enjoy a soft landing, and the bulls are happy to run with his narrative like they did in 2021. However, we’ve warned on numerous occasions that the Fed has always pushed the U.S. federal funds rate (FFR) above the peak year-over-year (YoY) percentage change in the core Consumer Price Index (CPI), and that nine of the last 10 bouts of rising inflation have ended with recessions

Therefore, while it may seem like our fundamental thesis is all about inflation and higher interest rates, it’s not. The important point is that nearly every rate-hike cycle ends with a recession, and economic malaises alongside high inflation are much worse.

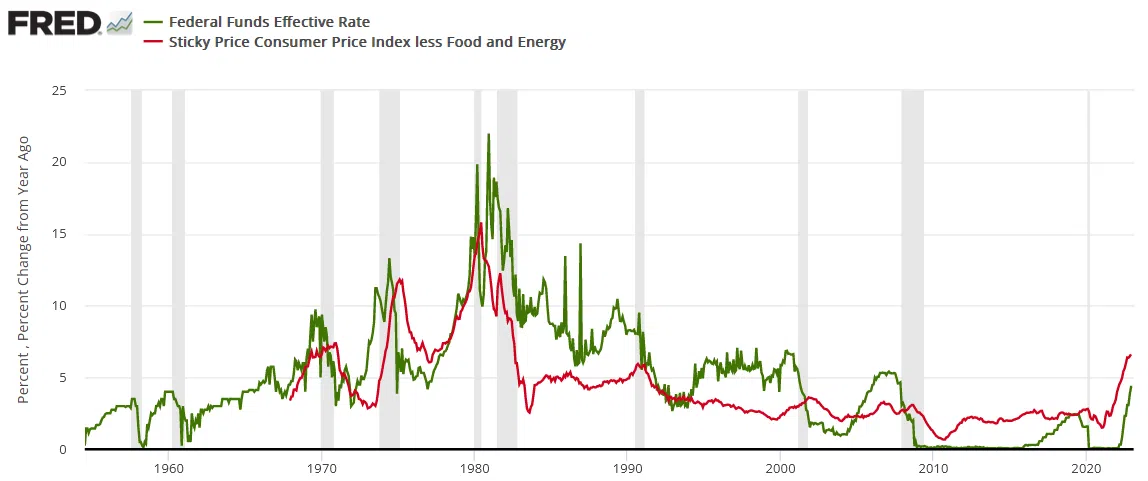

Please see below:

To explain, the green line above tracks the FFR, the red line above tracks the YoY percentage change in the core Sticky CPI (data starts in the late 1960s), and the vertical gray bars represent recessions.

If you focus your attention solely on the green line, notice how nearly all rate-hike cycles have ended with recessions since 1954? More importantly, please note that the FFR spikes in 1985 and 1986 were short term and occurred alongside a falling core Sticky CPI. Likewise, the FFR’s rise from 1993 to 1995 also occurred alongside a falling core Sticky CPI. As such, the inflation pressures were much lower and recessions were initially avoided before occurring later.

In contrast, the right side of the chart shows how the YoY core Sticky CPI has risen for 17 straight months. As a result, this is nothing like 1985 or 1993.

Consequently, the moral of the story is that we’re not betting against inflation slowing; we’re betting against a soft landing before it returns to 2%; and while the current sentiment makes it seem like a fairy tale ending is on the horizon, the historical data speaks for itself.

In other words, the bulls are betting against historical precedent and placing all of their hopes on Powell’s ability to accomplish something no Fed committee before him has. Would you make that bet? In reality, if Powell struggles to deliver a consistent message during his press conferences, he’s unlikely to engineer a soft landing.

From another angle, let’s break down Powell’s belief that he can tame inflation without a “significant increase in unemployment.”

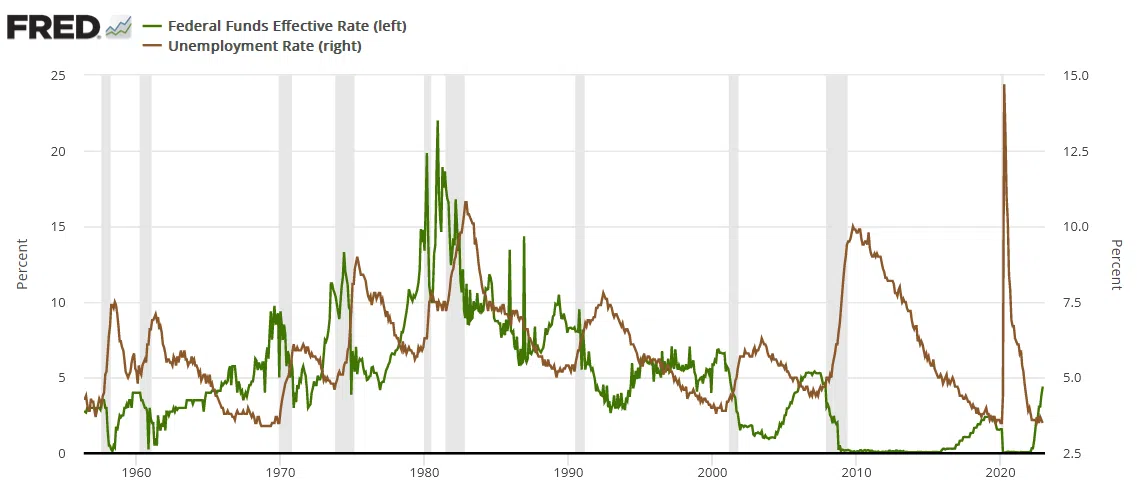

Please see below:

To explain, the green line above tracks the FFR, the brown line above tracks the U.S. unemployment rate, and the vertical gray bars represent recessions. If you analyze the relationship, you can see that nearly all rate-hike cycles end with recessions, spikes in unemployment, and as they unfold, the Fed cuts the FFR.

Conversely, the right side of the chart shows that the brown line is at a ~50-year low, while the green line is still rising. So, Powell and the bulls are ignoring the ramifications at their own peril, and it’s likely only a matter of time before the historical relationship returns.

Overall, inflation is only one-half of our bearish fundamental thesis. The second, a recession, is how the cycle should end. But, since the U.S. labor market is so strong right now, the second act is delayed, and that’s why we believe the FFR needs to rise more than expected.

It’s not because we think inflation will spiral out of control, but because the CPI can’t hit 2% when wages are running at 6%+. Therefore, the unemployment rate needs to rise to reduce wage inflation to 2%, and that means the FFR needs to rise to decrease consumption and decrease labor demand. Yet, none of this has happened, and that’s why the current narrative lacks credibility.

As it stands, the outlook for risk assets like gold is only bullish if you believe that history is irrelevant and Powell has figured out something that no Fed Chair before him has. We don’t.

How do you see the cycle ending: soft or hard landing? Why does the crowd put so much faith in Powell’s predictions? Do you believe the Fed can control the fundamentals?

Alex Demolitor

Precious Metals Strategist