While the recent Israel-Hamas turmoil helped boost the yellow metal, the domestic fundamental outlook is much less supportive.

Substantial Drawdowns Ahead

With inflation outperformance amplifying U.S. Treasury yields and the USD Index on Oct. 12, the PMs remained under pressure from their familiar fundamental foes. Moreover, while gold bounced due to geopolitical concerns in the Middle East, the fundamentals continue to follow our medium-term roadmap.

For example, investment heavyweight PIMCO released its Cyclical Outlook report on Oct. 11. And with the firm sharing our view that inflation is old news and weak growth is the next bearish catalyst, an excerpt read:

“We forecast core inflation in the 2.5%–3% area in the U.S. and Europe at the end of 2024. We anticipate that falling growth and rising unemployment will lead to more disinflation, helped also by other factors.”

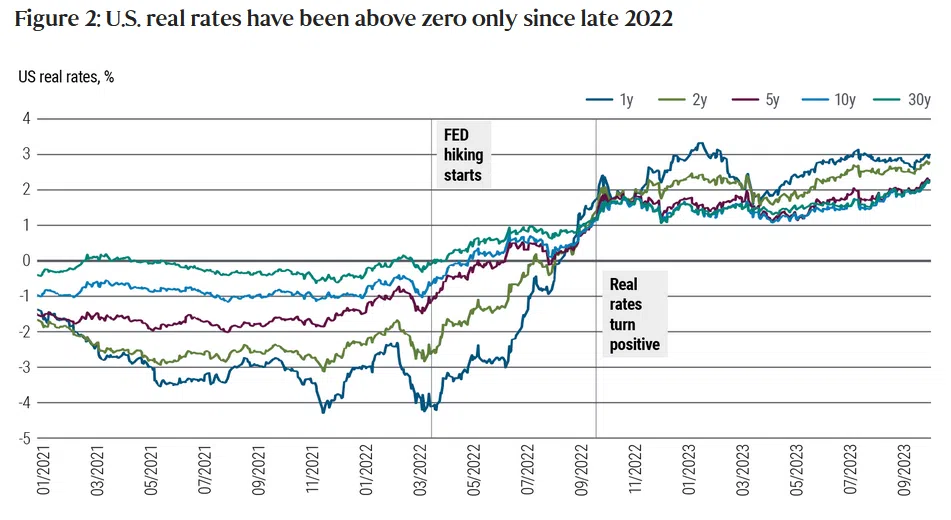

Please see below:

To explain, the colored lines above show how U.S. real yields remain positive across the curve and most recently made new highs when the rate surge unfolded. Moreover, we warned that non-transitory inflation would incite the Fed’s rate-hike campaign, which ultimately led to the uprising and weakness for assets like silver.

Furthermore, higher real yields have economic consequences, and those developments should cause problems in the months ahead.

PIMCO’s report added:

“We analyzed 140 tightening cycles across developed markets from the 1960s through today. When central banks hiked policy rates by 400 basis points (bps) or more – as several have done this cycle, including the U.S. Federal Reserve (Fed), the European Central Bank (ECB), and the BOE – almost all such instances ended in recession.”

Thus, while we warned that history is not on the soft-landing bulls’ side, most assets are priced as if inflation will dissipate with little economic carnage. And if (when) this narrative fails, the USD Index should soar, while the PMs should suffer substantial drawdowns.

Far From a Home Run

The housing industry is already sounding the recession alarm. We warned that higher long-term interest rates (not the FFR) are responsible for negative economic growth as mortgage, auto, and other credit vehicles become more expensive.

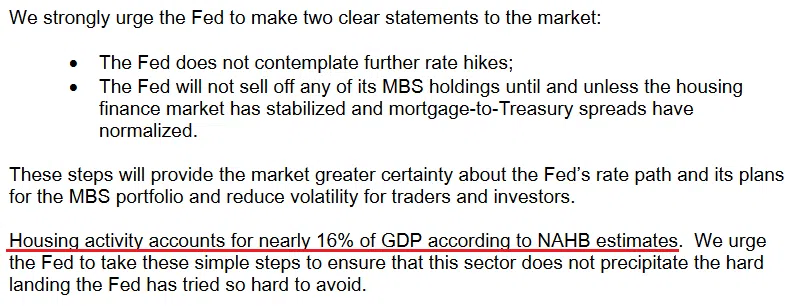

And with the National Association of Home Builders, the Mortgage Bankers Association, and the National Association of Realtors penning a letter to Fed Chairman Jerome Powell on Oct. 9 urging him to stop raising rates, it’s another indicator of the stress hiding in plain sight. The letter stated:

“According to MBA’s latest Weekly Applications Survey data, mortgage rates have now reached a 23-year high, dragging application activity down to a low last seen in 1996. The speed and magnitude of these rate increases, and resulting dislocation in our industry, is painful and unprecedented in the absence of larger economic turmoil….

“The uncertainty-induced mortgage-to-Treasury spread is costing today’s homebuyers an extra $245 in monthly payment on a standard $300,000 mortgage. Further rate increases and a persistently widespread pose broader risks to economic growth, heightening the likelihood and magnitude of a recession.”

Please see below:

So, while we warned these realities would occur, there is little the Fed can do to remedy the situation. First, it does not control the long end of the yield curve. Second, turning dovish will only exacerbate inflation. As a result, the longer long-term rates stay high, the more they will stress consumers and economic growth and increase the chances of a recession. As such, oil could be in big trouble over the medium term.

Finally, the FOMC released the minutes from its Sep. 19-20 monetary policy meeting. And while the commentary was balanced, an important statement read:

“All participants agreed that policy should remain restrictive for some time until the Committee is confident that inflation is moving down sustainably toward its objective.”

In other words, the Fed must remain hawkish to avoid another inflation spike, and economic growth should be the main casualty of their persistence. And as history shows, silver and mining stocks typically suffer the most when economic-induced volatility erupts.

Overall, another interest rate spike occurred on Oct. 12, and a sea of red confronted several risk assets. Yet, this means long-term interest rates will continue to suffocate the real economy, and the S&P 500 should crumble when the full effects become obvious.

To stay ahead of the crowd, subscribe to our premium Gold Trading Alert. We recently booked our 11th- straight profitable trade and have made money on both long and short positions in recent months. Plus, regardless of the PMs’ next moves, another attractive opportunity is approaching, which we think has the chance to generate immense profits. In other words, there’s never been a better time to join our community.

Alex Demolitor

Precious Metals Strategist