According to Jeremy Siegel, gold underperforms stocks heavily in the long run. However, it doesn’t mean we should throw it away from our portfolios!

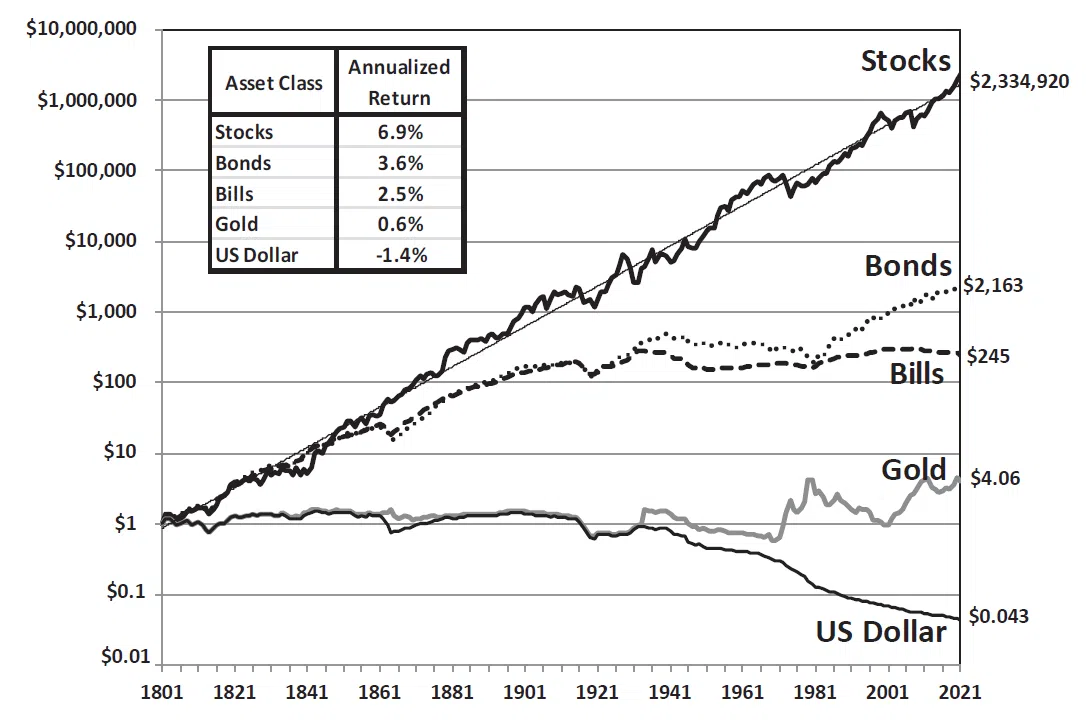

Not so much is happening in the markets right now. So why not talk about gold prices in the very long term? Recently, I’ve been studying a very interesting book, Stocks for the Long Run: The Definitive Guide to Financial Market Returns and Long-Term Investment Strategies by prof. Jeremy Siegel and I’ve come across the following chart:

It presents one of the longest series of data about investing returns in gold I’ve ever seen. As you can see, if you bought gold in 1801 by one dollar, it would be worth $94.32 at the end of 2021, which translates into a 2.1% average annualized geometrical rate of return. Not bad, but far from the returns achieved by bills or binds, not to mention stocks.

What’s worse, investing in gold would be even more disappointing in real terms. According to another chart taken from Siegel’s book, the real annualized geometrical rate of return for gold in 1801-2021 was, on average, 0.6%.

Hey, but shouldn’t gold be a good long-term investment? Well, the rate of return is low, but it’s positive, which means that gold protected investors from inflation over the long run. But the more important point is that Siegel’s figures don’t make much sense because, for most of the time presented we had the gold standard, in which the dollar was defined as a unit of weight of gold, so the price of gold in dollars was fixed and couldn’t appreciate.

Therefore, it is better to analyze the period after the end of the Bretton Woods’ system. The price of gold rose from $65 at the end of 1972 to $1,812 at the end of 2022. This equates to a nominal rate of return of 2,693% over 50 years, or an average of 6.9% per year (geometric mean), or 2.8% in real terms. Much better than 2.1% and 0.6% stated by Siegel!

However, before you buy a metal detector, please note that these returns could be overestimated. You see, under the gold standard, the free gold market was practically non-existent for years, and the price of gold was somewhat artificially low at a fixed level of $35 per ounce. When the gold window was closed, the price of the yellow metal skyrocketed, but it was a one-off event. Thus, I wouldn’t extrapolate past impressive results into the future, and I would say that the true average returns are probably somewhere between Siegel’s and mine estimates.

What Does It Mean for Gold as an Investment Asset?

Does the fact that gold underperforms stocks significantly mean that it’s a poorly performing asset that should be excluded from investment portfolios? Not at all! It just confirms that gold shouldn’t be bought as a long-term engine of growth but as an investment portfolio diversifier and a safe-haven asset.

You see, stocks should be the growth engine of each portfolio. They should outperform commodities in the long run. If the shares of productive companies grow less than yellow rocks, it would be strange, actually.

In other words, when you buy gold, you could expect a small but positive real rate of return, so it will keep pace with inflation and add something more. Besides, it will serve you as insurance for the remainder of your investment portfolio. Additionally, you can invest in gold in order to benefit from the cycles in the precious metals market. This leads us to the next section.

Implications for Gold

What does it all imply for the gold (and silver) market in 2023? Well, last year gold ended about flat, which means that it lost some value in real terms. However, since November, the yellow metal has been in an upward trend, as the chart below shows (courtesy of goldpriceforecast.com). As skeptics argue, it might be just a short-term move within a broader bearish wave.

However, the macroeconomic backdrop – namely the slowdown in inflation and in the pace of the Fed’s hikes in the interest rates – suggests that a new bull market in gold could have already started. If this is true, it would be an additional argument for purchasing some gold – not only as long-term insurance but also as a medium-term investment.

Arkadiusz Sieron, PhD