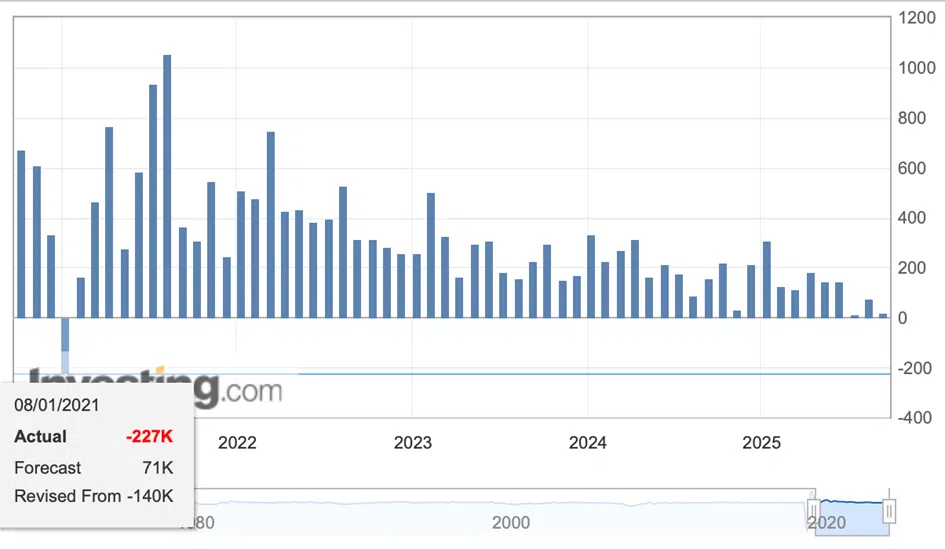

The nonfarm payrolls are bad, and – what’s more important – they are much worse than expected.

The forecast was 75k. We got just 22k. This is terrible.

It’s not a one-time thing, either. That’s the worst three-month average in a very long time. The previous significant declines in the nonfarm payrolls were just single-time events, but this is different. This shows the shift in what’s happening in the U.S. economy. The tariff effects start to arrive in their full “glory”.

Trouble on the horizon, Fed about to be cutting rates… Doesn’t it remind you of something?

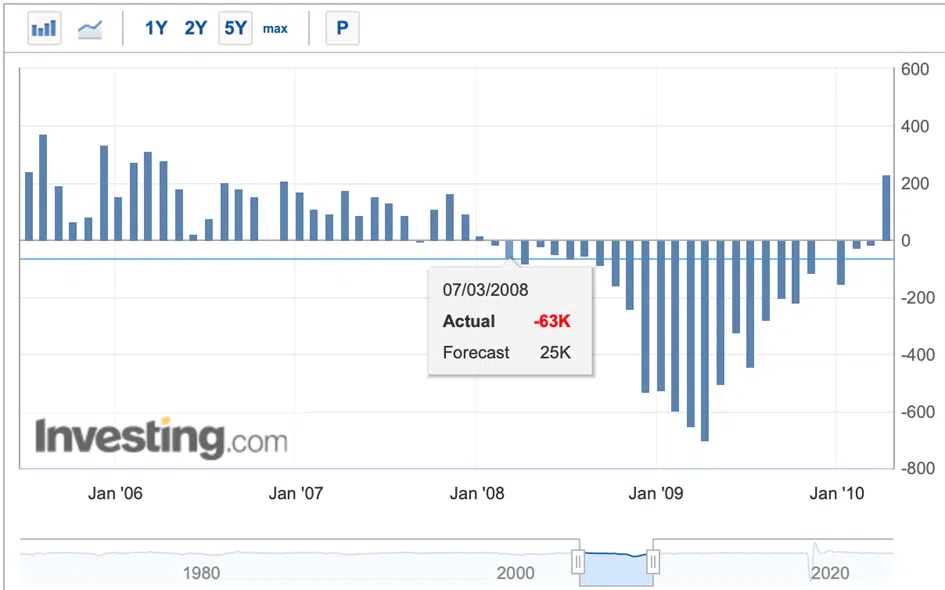

Well, I kind of spoiled this with the title. Yes – that’s what we saw in 2008.

The time when it was clear that we had a major problem in 2008 was March 7. That’s what gold was doing at that time.

A quick rally followed and then a big, 30% decline.

Of course, that was a 30% decline only in gold – the slides in silver, miners, copper, and FCX were not so small – they were extreme.

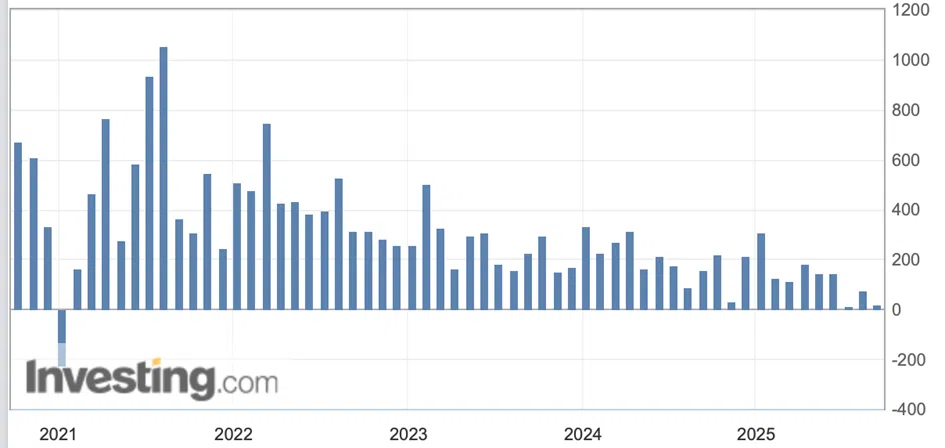

And that single-time drop in nonfarm payrolls at the beginning of 2021?

That’s what preceded a sharp slide as well.

Gold moved higher today, but… that’s what it also did in the short term in 2008 after a similar nonfarm payroll report.

Silver moved up but ended the session almost unchanged. The move higher in platinum was also tiny compared to yesterday’s 5%+ decline.

The USD index's situation was different in 2008 than it is now. Back then, it was before a broad bottom, and now it's already after it. That's a reason due to which the USDX could rally earlier, and gold could decline earlier than in 2008. That rally that we saw after March 7, 2008 in gold – it might not happen this time. Or perhaps it already happened in today’s early-market trading.

All this – plus knowing what happened when rates were cut in 2008 – further confirm that the rally in the precious metals market is likely ending here or that it has already ended. I previously ended the analysis by stating the following:

Very important employment numbers are going to be released tomorrow, and they could trigger a reversal in the precious metals market – even if they are weak and they confirm the case for lower interest rates. Given that gold just made headlines, and given how extremely overbought mining stocks are, we might have the ‘buy the rumor, sell the fact’ type of reaction.

This remains very much up-to-date – a rate cut could be the final trigger for the decline – if we don’t see it by that time.

Is This Really It? Or Are We Waiting for Something That Never Comes? Should You Still Trust My Analysis?

Here’s something that I think should be addressed – just how much trust can you place in my analysis – at all?

There were several comments on Golden Meadow® that mentioned my past performance and asking me to comment on it. Some were published as they followed our kindness of speech rule, and some did not, as they were not in line with it, or they disclosed what’s only available to premium subscribers. To clarify, it’s perfectly fine to disagree with someone (myself included) – what’s not ok is being mean or to trigger panic among fellow investors. There is a certain standard of discussions that I aim to keep on the platform. Sadly, many comments of people that post after the market moves against my forecasts, fall into one of those two latter categories. Anyway, I think this matter should be discussed.

I’ve been expecting a huge slide in gold, silver, and mining stocks to come since 2013 (shortly after the slide started). Years have passed, and while this turned out to be a great idea to be out of the market with the long-term capital for several years, it didn’t work in the end, as I was not satisfied with the sizes of declines and waited for a bigger one. I wanted to time this purchase perfectly for you, and it seems that I cared too much. I got biased and I didn’t let go of the idea that the bigger decline was coming. Some might call me a man of consequence, and some will call me stubborn. Some will find worse names. You be the judge.

Either way, it was only last year when I wrote about getting back with half of one’s investment capital in case of the silver bonds. Given what silver did since that time (and its great long-term potential), those who invested in it are likely very happy with that decision. I did write about getting back to gold nor mining stocks with the other half of capital, though.

What might be the biggest reason for one to doubt my ability to time the precious metals market, though is the currently open position in the GDXJ – which was opened with GDXJ still below $40. The decision to keep this position open for so long was the worst thing in my 20-year investment career. Should you trust someone, who made such a big mistake on the current trade? You be the judge. It might have been fair to balance this with some comments about previous profits or how great my performance was in some of the years where I had almost only profitable calls or something like that, but I think that I’ll leave it at that.

Is this trade still worth following right now? Again, you be the judge – I’m presenting the situation exactly as I see it. You know, there is this tendency for people to give up on certain trades right before they are about to turn around. The bull markets end when the last bear gives up. Am I giving up? Perhaps me writing this, and you reading this is something that can also work in this way – as a proof that something has shifted.

I’ve given up on “insisting” that gold, silver, and mining stocks “have to” decline here. But I’m not changing my mind regarding the trade – the time of the year and the extent of the rally are very strong indications that this is either the top or were very close to it. But again… You be the judge.

Not everything went bad, though. Truth be told, if one followed what I’ve been writing to the letter, they should be in the green, nonetheless.

How come?

The insurance part of the portfolio. The insurance against systemic risk. And the insurance of anyone – myself included – being wrong with regard to timing.

The insurance part of the portfolio is something that I kept intact at all times. The portfolio report to which I’ve been linking over the years (I recently updated this, but the core part remains intact) featured three sample portfolios: Eric’s (beginner’s), John’s (trader’s), and prof. Jill’s (long-term investor’s). Scroll the above-linked page until you see the first image. (You may want to review the “Position Sizes’ section in that report as well. Or read more about it in the separate section “Beginner’s Guide to Gold Trading” - it even includes a simulation of what happens at different position sizes – I strongly suggest reading that.)

The insurance parts (the part about which I’ve been writing to keep invested at all times (in physical gold and physical silver, ideally geographically diversified) were:

- 44.1% in the beginning investor’s case (29.4% in gold and 14.7% in silver)

- 17.6% in trader’s case (6.5% in gold and 11.1% in silver)

- 33.6% in long-term investor’s case (17.1% in gold and 16.5% in silver)

The link to this report has been present in all premium analyses that I’ve been posting for over a decade, a few times in each analysis. Some subscribers saw the link thousands of times.

Why am I writing this? Because this section of the text is not about self-flagellation; it’s about providing you with facts, so that you can make the most informed decision about the current outlook, and the trading/investment decisions that you can make.

Because those decisions are and will always remain your responsibility. Even if you choose to use the service of an investment advisor or money manager – guess, who is still responsible for choosing them and is making the decision to appoint them? It’s still you.

Hiding or ignoring the fact that I not only developed, but then continuously featured and promoted framework dedicated to protecting your and others’ capital in case I’m (or someone else is) wrong about a certain trade or investments, as well as neglecting to say that my framework suggests keeping between 17.6% and 44.1% of one’s capital in physical gold and silver at all times – that’s simply misleading and it misrepresents my performance and gives incorrect impression about the quality of my analytical work and the level of care that I put in all this.

That huge loss in GDXJ or any other asset is only huge if you ignore what I’ve been repeating thousands of times about position sizes. Max loss per trade in the portfolio report? Between 0.1% and 2% of capital. I did use to write about a big position size (even up to 300% of the regular position size), which still means max loss 0.3% - 6% if the portfolio instructions were followed to the letter.

What happens if you use the entire 6% to buy JDST and it declines very significantly? You lose not more than that 6%. And when you combine that with the 17.6% - 44.1% allocation to gold and silver, where the first has more than doubled, what you get in total? Profits. And you know what? There were also multiple profitable trades since 2013.

So, there you have it – a full disclosure of what happened and when, and what I currently think about the market.

If you prefer to judge the value of my analyses based on the GDXJ (or other) trade – you are free to do so.

If you prefer to take the whole picture into consideration – you are also free to do so.

You are also free to blame me or someone else for your investment decisions, and you are free to take ownership thereof. One of those will put you in the position of strength and the other will put you in the position of a victim – again, it’s your call. If you never read my portfolio report and you chose to selectively apply parts of my analyses, then you are free to still blame me for… whichever part of the above you see fit, and you are free to treat any of the above as a reminder that paying attention to position sizes and portfolio structuring is a foundation of successful investment process.

And since I’m already discussing the big picture, I would also like to show you what I’ve been doing recently, why, and tell you what I’m going to do next.

You see, the tragic fact about not getting back in the gold on time and the recent GDXJ trade is that they are both connected to me caring too much about the outcome. Not because of my ego – that has actually never been an issue for me, being wrong every now and then is an integral part of being a human being especially if one is dealing with markets. It’s the perfectionism combined with care that apparently was the problem.

The ego wouldn’t interfere with me taking a break from the markets and work in general, but the combination of latter… Let’s just say that I don’t even remember when I took real time off from work longer than a week. I haven’t taken any this year, and I think I haven’t taken more than a few days last year.

When I had started writing my premium analyses many years ago, I did it once per week, and I didn’t spend a lot of time on the market analysis. I didn’t get caught up in all the short-term price fluctuations. I just shared what I found interesting, without the pressure to explain the daily price movements. Looking back – I should have stayed with that format, because it simply worked.

With big, daily reports and with the mission to create something bigger than just a newsletter, the pressure started to mount. I wanted to give you absolutely the best, and I didn’t want to accept anything else. Not because of my ego, but because of the standard of service that I aimed to provide you with. The paradox is that the more one wants the trade to work, the less it tends to do that. But you know that from your own trades as well – that’s how people get biased.

Don’t get me wrong – the care itself is nothing wrong. The market analysis is the only place where it can be an obstacle. There are multiple other places where I utilized it. For example:

- I wrote a completely new portfolio management strategy which has some parts that I’m particularly proud of (the tactical time-out after losing a significant part of one’s capital, for example)

- I designed the portfolio calculator, which is yet another tool that I aimed to use to motivate everyone to keep their position sizes intact and their portfolios balanced

- I designed the portfolio simulator – which aims to do the above through gamification (I’m surprised by the lack of feedback on it, I thought it would be not just educational, but also fun to engage in this simulation)

- I even designed a tool specifically addressing the current GDXJ trade as – based on individual correspondence – it seemed that some people might have enormous positions in JDST that they would not want to close despite them being obviously too big. I created a tool helping to hedge the position with gold based on two scenarios that seemed most likely to me at that time.

Where do we go from here?

Fortunately, I have solution regarding the “care paradox”, and it’s already being implemented. As I want to deliver the best analysis to my subscribers – and since apparently, I haven’t been able to do that in person this year – I’m introducing more and more experts to Golden Meadow® and I’m providing access to their services through Diamond Package. If I can’t provide the best myself, then I’ll create a service that will provide it, anyway.

There’s also something that I’m adding to the Diamond Package - it’s a special newsletter, in which I will cover the performance (transparent, clear analysis, not hype) of experts included in the package and comment on how to – in my view – best take advantage of their analyses, trades, and signals. There is also a special project underway that’s about detecting bias in a given analyst’s work (effectively protecting you and everyone else from what I discovered in my own analyses).

This way, the number of experts included in the Diamond Package will not be overwhelming, but useful. And this will be even more important going forward as I’ll aim to onboard more experts on Golden Meadow® (especially ones covering gold, commodities, and – by popular demand – options), and have their services also featured in the Diamond Package.

Yes, this also means covering my own performance in a clear, transparent way regardless of it looking good in comparison to others or not.

I’m talking to many of those experts on a regular basis, I can see what’s going on in their analyses and approaches, and I can generate a ton of value thanks to this “insider information”. The “downside” is that this service is and will need to be provided at a premium price, but if you’ve been a subscriber to my Gold Trading Alerts in the past, please reach out to us, and perhaps we can create an offer that would suit you.

The beauty of this situation is that since I know that there’s an entire team of experts providing great (I checked their methodology / performance) services, and that those following them (and me) will likely be fine regardless of a single or several wrong trades in anyone’s (including my own) own premium service, I can remove a large part of the above-mentioned pressure, thus restoring my regular performance.

There’s more to Golden Meadow® than the above, but that’s where things will start.

If you’re willing to give the Diamond Package a chance (and it’s more than worth it), there’s currently a two-week trial that you might use to conveniently do that.

If not, and if you’re sick and tired of whatever I’m writing or doing, then you’re also free to choose not to follow anything else from me.

I might give up on this trade, but I’m not giving up on my care, and I’m not giving up on providing the best to you.

If this level of transparency is refreshing to you, you'll appreciate the weekly Diamond Package performance reports where I'll rank myself against all other experts - whether I'm #1 or #12.

Thank you.

Przemyslaw K. Radomski, CFA

Founder, Golden Meadow®