Will bearish seasonality keep risk assets on their back foot?

With the S&P 500 reversing sharply intraday on Jan. 18, we warned before the open that seasonality made the short-term outlook highly unattractive. We wrote:

S&P 500 seasonality often turns in mid-January, and the negativity persists until the end of the month….. Overall, while the fundamental backdrop has always been bearish, the sentiment setup also supports lower precious metals prices. Consequently, we view the risks as heavily skewed to the downside, especially for silver and mining stocks.

Thus, with silver and mining stocks suffering the brunt of investors’ wrath, the January blues arrived on cue. But, with gold only down modestly on the day, the yellow metal demonstrated relative strength. However, with the crowd misjudging the fundamental backdrop and assuming that rate cuts will commence in the months ahead, Fed officials continue to maintain their hawkish stance.

For example, Richmond Fed President Thomas Barkin said on Jan. 17:

“You just can’t declare victory too soon…. I want to see inflation, and median and trimmed mean, compellingly headed back to our target. As long as inflation stays elevated, we need to continue to move the needle, to tighten if you will, ever more.”

Likewise, Philadelphia Fed President Patrick Harker said on Jan. 18:

“High inflation is a scourge, leading to economic inefficiencies and hurting Americans of limited means disproportionately.” The Fed's “goal is to slow the economy modestly and to bring demand more in line with supply.”

He added:

“Hikes of 25 basis points will be appropriate going forward…. I expect that we will raise rates a few more times this year.”

In addition, Cleveland Fed President Loretta Mester said on Jan. 18:

“We’re beginning to see the kind of actions that we need to see,” but “I still see the larger risk coming from tightening too little.”

As a result, she reiterated her commitment to a 5%+ U.S. federal funds rate (FFR).

Please see below:

Source: Reuters

Source: Reuters

Continuing the theme, St. Louis Fed President James Bullard said on Jan. 18:

“Why not go to where we're supposed to go? Why stall…? Let's move the policy rate to the right level” and “see how 2023 unfolds.”

Therefore, he prefers “frontloading” rate hikes so that the FFR can reach the 5.25% to 5.5% range sooner rather than later.

Please see below:

Source: Bloomberg

Source: Bloomberg

Adding her voice, Dallas Fed President Lorie Logan said on Jan. 18:

“I see elevated services inflation as a symptom of an overheated economy, particularly a tight labor market, which will have to be brought into better balance for the overall inflation rate to return sustainably to 2%.”

Furthermore, she advocated for continued quantitative tightening (QT):

“With the [standing repo facility] as a backstop and the power of market incentives to redistribute liquidity, I am confident that we have room to continue running off our assets for quite some time,” Logan said. “We’ll need to watch the outlook and adjust our balance-sheet strategy appropriately so that liquidity levels don’t fall too low.”

Consequently, while Fed officials remain aligned in their hawkish expectations, investors are pricing in rate cuts in mid-2023. Moreover, not only does the crowd expect a dovish 180, but they don’t even expect the peak FFR to reach 5%. As it stands, an epic battle is underway, and investors have called the Fed’s bluff.

However, we warned on Dec. 16, 2021, that Chairman Jerome Powell’s deputies are often leading indicators of future Fed policy. We wrote:

As one of the most important quotes of the [post-FOMC] press conference, [Powell] admitted:

“My colleagues were out talking about a faster taper and that doesn’t happen by accident. They were out talking about a faster taper before the president made his decision. So it’s a decision that effectively was more than entrained.”

And while Powell sounded a little rattled during the exchange, his slip highlights the importance of Fed officials’ hawkish rhetoric. Essentially, when Clarida, Waller, Bostic, Bullard, etc., are making the hawkish rounds, “that doesn’t happen by accident.” As such, it’s an admission that his understudies serve as messengers for pre-determined policy decisions.

More importantly, the fundamentals support the Fed’s view, and the crowd likely has it wrong. In 2021, when investors and the Fed were aligned in their “transitory” beliefs, we warned that stubborn inflation would lead to a material increase in interest rates; and now, we’re aligned with the Fed, and the crowd is the lone wolf.

But, not only does history show that interest rates are too low to win this inflation fight, but near record wage growth (according to the Atlanta Fed) and a ~50-year low unemployment rate are not indicative of demand destruction. Therefore, when investors overreact to soft economic data, they miss the forest through the trees.

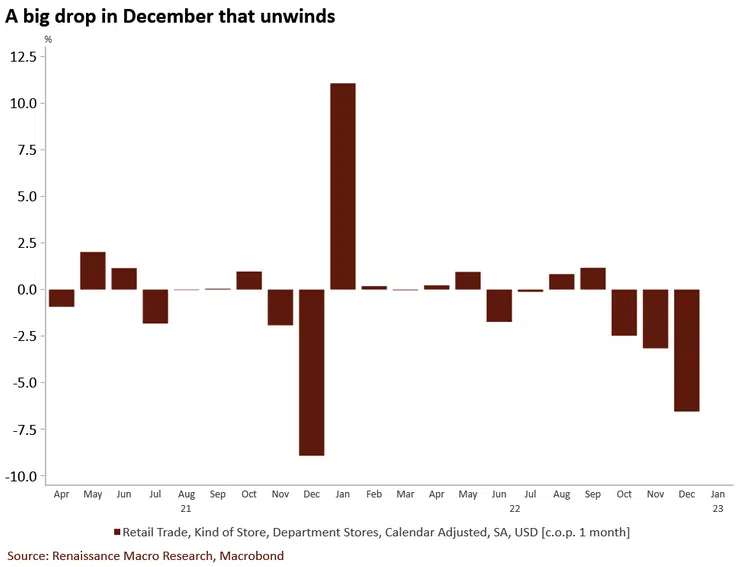

Please see below:

To explain, U.S. retail sales came in weaker than expected on Jan. 18, and the brown bars on the right side of the chart above show a sharp month-over-month (MoM) deceleration in department store retail sales

Yet, if you analyze the middle of the chart, you can see that while sharp pullbacks were present in November and December 2021 (combined), the weakness reversed materially in January 2022; and while seasonal adjustments often skew the data, the current weakness should show a bullish reversal in the months ahead.

Also noteworthy, when the Fed hiked the FFR rapidly in 2022, the U.S. housing market was the most affected, as higher long-term interest rates increased mortgage rates; and while the crowd opined that a crisis was on the horizon, the sector weathered the interest rates storm.

Furthermore, now that long-term Treasury yields have declined, the housing dip buyers are back, and it's another indicator of why demand destruction has not reached the levels necessary to win this inflation battle.

Please see below:

To explain, U.S. mortgage applications spiked by nearly 28% week-over-week (WoW), the largest WoW increase since March 2020. Likewise, if you analyze the orange horizontal dashed line, you can see that the weekly jump was one of the largest in more than 12 years.

As a result, whenever the crowd assumes that small inflation progress means the war is over, the loosening of financial conditions only spurs more demand (like with mortgage applications) and makes the Fed’s job more difficult. Thus, the consensus is highly uninformed about the historical implications of how inflation behaves, and how it’s finally resolved.

Overall, the gold price sidestepped much of the carnage, but the fundamentals remain highly bearish. With the crowd expecting the Fed to cut interest rates in roughly six months, their front-run optimism is the opposite of what the Fed wants. Consequently, due to the contrasting fundamentals, we believe the motto of ‘don’t’ fight the Fed’ is warranted in this instance.

But, let us know what you think: where do you see the FFR going? Should you trust the bond market or the Fed? And why is the crowd so happy to ignore the historical lessons about inflation?

Alex Demolitor

Precious Metals Strategist