Some lessons to be learned on why you should double check your sources before making trading or investment moves.

With the S&P 500 selling off into the close on Nov. 14, the general stock market took a breather from its recent sprint higher. Moreover, with gold, silver and mining stocks ending the day mixed, investors are waiting for the next fundamental catalyst.

However, with misguided narratives guiding them in the wrong direction, rhetoric from ZeroHedge continues to lead the crowd down an unprofitable road. For example, the latest musing has the Fed increasing its inflation target to 3%, and the article cites the familiar arguments that the Fed can’t tolerate a recession or high employment, so it will let inflation rage.

Yet, while each upload may seem like a fresh take on the fundamentals, please remember that ZeroHedge is a broken clock when it comes to pivot predictions. To explain, I wrote on Oct. 27:

Source: ZeroHedge

Source: ZeroHedge

So, while ZeroHedge has amplified the false pivot narrative for much of 2022, imagine if you had bought the PMs in January. You would have suffered major losses.

While the site proclaimed that “U.S. GDP growth is now rapidly collapsing” in January, it’s been several months, and the Atlanta Fed raised its Q3 real GDP estimate to 3.1% on Oct. 26. Thus, it’s prudent to pay less attention to narratives and more attention to the data

To that point, Q3 real GDP came in at 2.6%, and the Atlanta Fed has a 4% prediction for Q4 (made on Nov. 9). Consequently, if you positioned for ZeroHedge’s pivot warning and bought the GDXJ ETF in late January, you would have suffered substantial losses , even considering the recent rally.

Please see below:

Overall, the moral of the story is to scrutinize where the information comes from; and while ZeroHedge has useful data, its analysis is biased. Therefore, if you take its conclusions at face value, you may be disappointed with the results.

In addition, you can’t reverse engineer a stable economy. With inflation still unanchored, a Fed that listens to ZeroHedge will only make a bad situation worse. As a result, while investors assume that a cautious central bank is bullish, they’ll realize in hindsight that it creates more problems than it solves.

Furthermore, please remember that false optimism is nothing new to those that understand the fundamentals. For example, Michael Hartnett, Chief Investment Strategist at Bank of America, told clients on Nov. 11:

“’Inflation shock’ is over, but 'inflation stick' of briskly rising services and wage inflation is here to stay; inflation will come down but to remain above range past 20 years.”

As such, while I’ve warned repeatedly that the Fed’s inflation fight will be one of attrition, Hartnett still sees the S&P 500 hitting ~3,000 in 2023. That means the investors expecting a sustainable pivot and low inflation are living in la-la land.

Please see below:

Source: Reuters

Source: Reuters

Also, while ZeroHedge insinuates that a crashing U.S. economy will let the Fed pivot and push asset prices to new highs, the reality is that resilient growth and employment coupled with high inflation are bullish for the U.S. federal funds rate (FFR); and unless all three collapse, the idea of rate cuts is ridiculous.

Please see below:

Source: Reuters

Source: Reuters

Likewise, please remember that investors are often the most bearish at the bottom and the most bullish at the top. Thus, while the PMs and the S&P 500 have enjoyed material rallies, their ascents make it more challenging to sustain the optimism.

Please see below:

Source: CNN

Source: CNN

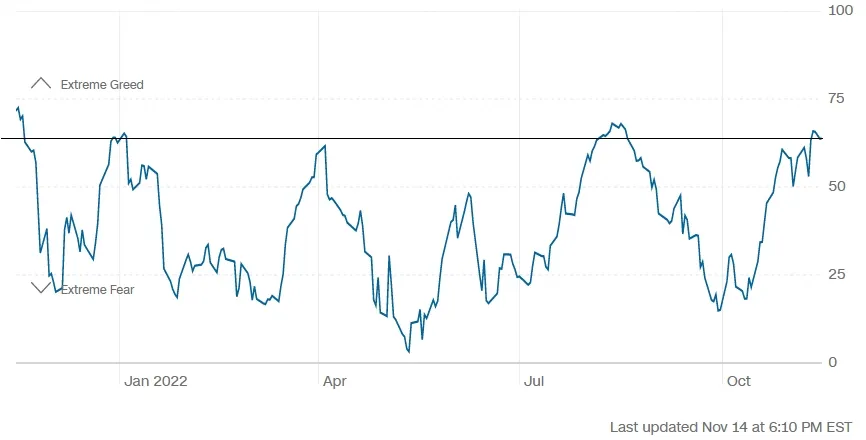

To explain, the blue line above tracks CNN’s Fear & Greed Index. For context, the metric is a contrarian indicator, and high values are considered bearish. If you analyze the right side of the chart, you can see that the metric is at one of its highest levels in 2022.

Moreover, before the S&P 500’s decline on Nov. 14, it was only two points below its 2022 high; and while extreme fear was present in early October, sentiment has shifted and greed reigns.

However, while seasonality is bullish for the S&P 500, the fundamentals are bearish, and the crowd should find it difficult to sustain higher prices without the fundamental support. So, while sentiment can keep gold, silver, mining stocks and the S&P 500 uplifted in the short term, the peaks and troughs in the blue line above highlight how quickly things can change.

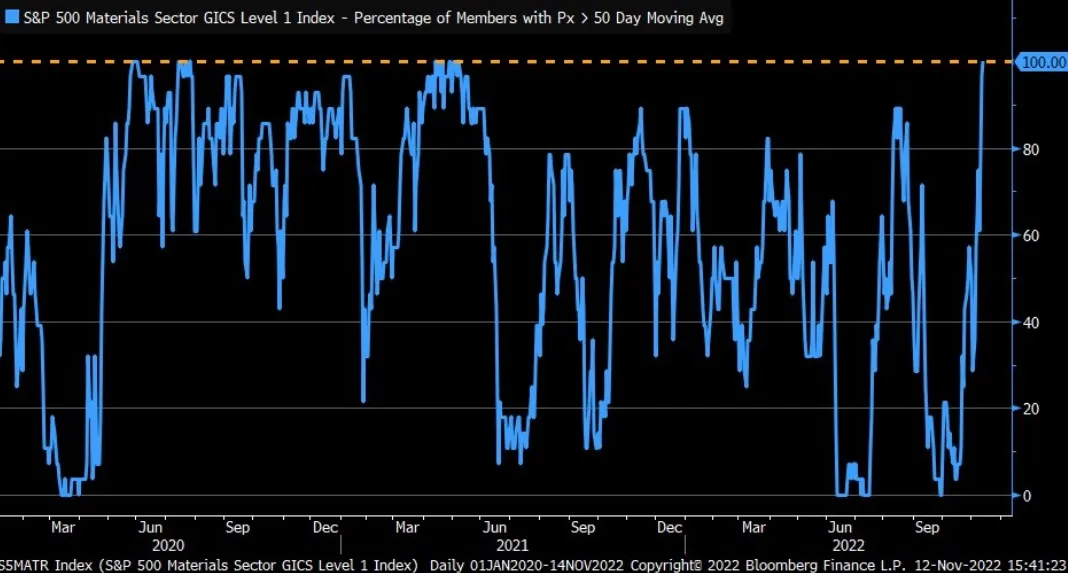

As further evidence, while CNN’s Fear & Greed Index signals greed, though, its still below extreme greed, the materials sector is on another level.

Please see below:

To explain, the blue line above tracks the percentage of companies in the materials sector trading above their 50-day moving average. For context, metals and mining make up roughly 14% of the sector. If you analyze the right side of the chart, you can see that the figure stands at 100%, which is a sizable shift from the 0% present in late September.

As a result, the data highlights why we’re likely much closer to the top than the bottom; and notice how abnormally high and low readings are nearly impossible to sustain? This is because periods of too much pessimism and optimism often revert to the average when investors take a thoughtful look at the fundamentals.

Therefore, since the metric can’t go any higher, a material reversal should result in substantial declines for gold, silver, and mining stocks over the medium term.

Reality Checks

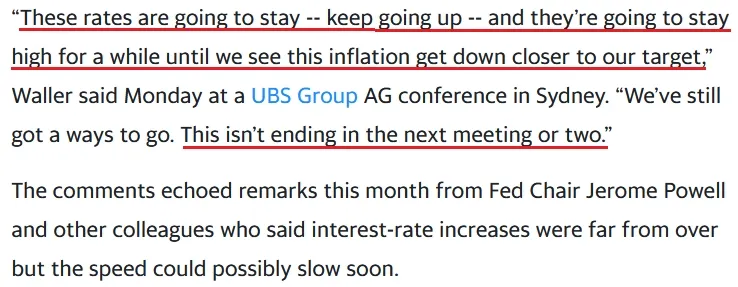

While investors are known to buy hope and sell reality, Fed Governor Christopher Waller said on Nov. 13:

“We’ve got to see [rate hikes] continue because the worst thing you can do is stop [tightening financial conditions] and then [inflation] takes off again, and you’re caught…. This is exactly the situation we had gotten into in July.”

He added:

“I can’t speak for [Fed Chairman Jerome Powell], but as I watched the press conference, that was the signal: to quit paying attention to the pace and start paying attention to where the end point [FFR] is going to be. Until we get inflation down, that endpoint is still a ways out there.”

As such, while the crowd thinks they can create their own reality, the fundamentals guide the Fed, and the Fed has a substantial inflation problem.

Please see below:

Source: Bloomberg

Source: Bloomberg

Also, Fed Vice Chair Lael Brainard said on Nov. 14:

“I think it will probably be appropriate soon to move to a slower pace of increases, but I think what’s really important to emphasize is... we have additional work to do.”

Thus, while Brainard is known for her dovish disposition, a data-dependent approach is no different than officials’ stance in 2021. In a nutshell: if inflation recedes, they’ll stop hiking. If not, they won’t. However, with inflation still materially underestimated, the Fed’s conundrum is far from priced in.

For example, Brainard added:

“We have raised rates very rapidly... and we’ve been reducing the balance sheet, and you can see that in financial conditions, you can see that in inflation expectations, which are quite well-anchored.”

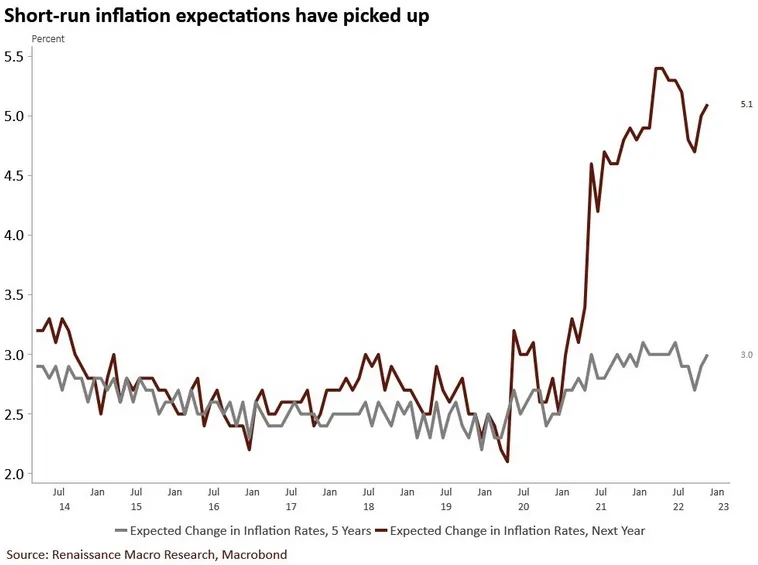

Yet, I noted the re-acceleration of inflation expectations earlier on Nov. 14. I wrote:

To explain, the brown line above tracks Americans’ 12-month inflation expectation, while the gray line above tracks their five-year forecast [University of Michigan data]. If you analyze the right side of the chart, you can see that both metrics have risen recently, which highlights the stickiness of inflation psychology. So, while the crowd assumes the war is over, the reality is that the Fed has made little progress in solving the problem.

Furthermore, Fed Chairman Jerome Powell said during his press conference on Nov. 2:

Source: U.S. Fed

Source: U.S. Fed

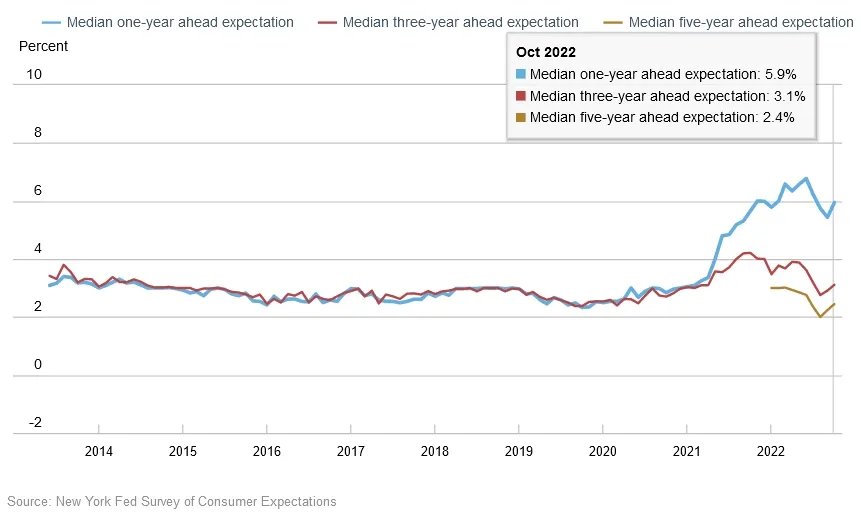

Well, the New York Fed released its Survey of Consumer Expectations (SCE) on Nov. 14, and the jump was similar. The report stated:

“Median one-and-three-year-ahead inflation expectations increased to 5.9 percent and 3.1 percent from 5.4 percent and 2.9 percent, respectively. The median five-year-ahead inflation expectations, meanwhile, rose by 0.2 percentage point to 2.4 percent.”

Please see below:

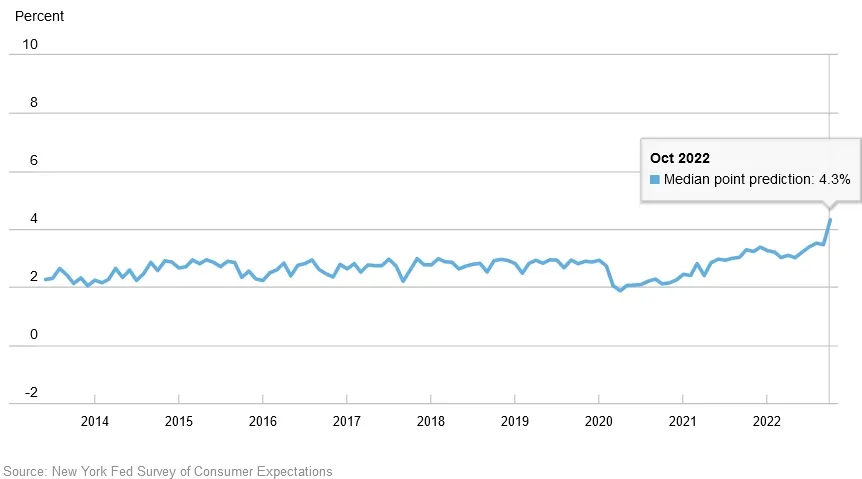

More importantly:

“Household income growth expectations touched a series high of 4.3 percent, up from 3.5 percent in September.”

Please see below:

In addition:

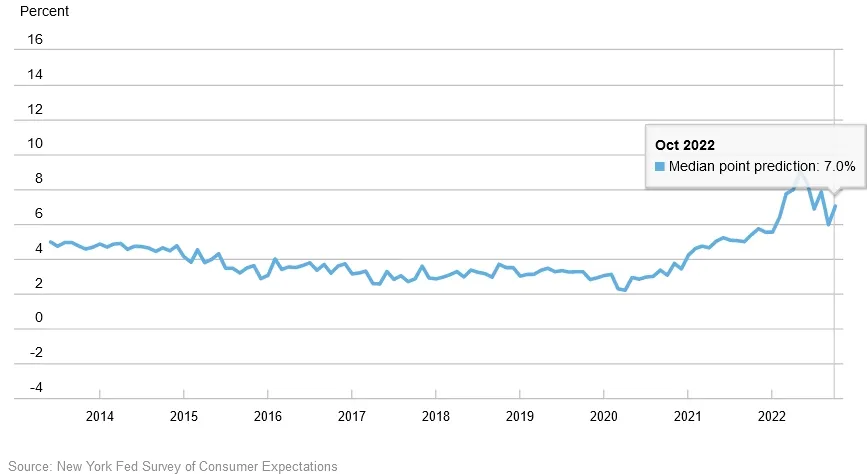

“Median household spending growth expectations increased to 7.0% from 6.0%.”

Please see below:

Thus, with Americans’ income, spending and inflation expectations rising in October, does this seem like an environment that supports a dovish pivot? Moreover, the latter two metrics are well above their pre-pandemic highs, and I warned repeatedly that record-high checkable deposits and robust wage inflation has Americans flush with cash. Therefore, their ability and willingness to spend should keep the Consumer Price Index (CPI) elevated for much longer than the consensus expects.

The Bottom Line

While the crowd and ZeroHedge jump from one narrative to the next, our fundamental message has been consistent: reducing inflation is extremely difficult, and history shows that every inflation fight since 1954 has ended with a recession. Plus, the periods where the Fed turned dovish amid high inflation (“stop-go” monetary policy) resulted in even worse outcomes for the U.S. economy and the S&P 500. So, while the consensus assumes the Fed can achieve the near impossible, history and the current data suggest otherwise.

In conclusion, the PMs were mixed on Nov. 14, as the GDX ETF ended the day in the red. However, the USD Index and the U.S. 10-Year real yield increased, and more upside should materialize in the months ahead. As a result, we believe gold, silver and mining stocks have not seen their medium-term lows.

Alex Demolitor

Precious Metals Strategist