The bulls have pushed the gold price to an unsustainable level.

Seasonality and short-covering had investors in an optimistic mood on Dec. 21, even as the fundamentals continue to deteriorate. Moreover, while the current narrative suggests that the U.S. federal funds rate (FFR) is near its peak and rate cuts will commence in 2023, North American central banks are far from solving their inflation problem.

For example, we noted that due to their geographical proximity and trade relationship, the U.S. and Canada often enact similar monetary policies; and with Canadian inflation remaining resilient in November, the Bank of Canada’s (BoC) expectations contrast the fundamental realities. To explain, we wrote on Dec. 8:

While the BoC cited “excess demand” and “unemployment near historic lows,” and in the next breath, questioned “whether the policy interest rate needs to rise further,” the contradiction highlights the conundrum confronting North American central banks. With some areas of their economies running too hot, while others are too cold, they want to have their cake and eat it too.

However, the reality is that supporting growth encourages inflation, and history shows the gambit ends in a recession regardless of what they do; and while the BoC (and maybe the Fed next week) thinks the overnight lending rate could peak at 4.25%, we believe the central bank materially underestimates the challenges that lie ahead.

To that point, the Canadian Consumer Price Index (CPI) came in at 6.8% year-over-year (YoY) on Dec. 21 and outperformed the consensus estimate of 6.7% YoY.

Please see below:

Source: Investing.com

Source: Investing.com

Furthermore, the official press release showed that inflation accelerated across five of the eight components.

Please see below:

Source: Statistics Canada

Source: Statistics Canada

To explain, the dark blue bars above show that food, shelter, household, health and alcohol/tobacco products were more expensive on a YoY basis in November. As a result, while the overall CPI declined by 0.10%, "gasoline prices fell 3.6% in November following a 9.2% increase in October."

In addition, "excluding food and energy, prices rose 5.4% on a yearly basis in November, following a gain of 5.3% in October." Thus, Canada's core CPI increased in November, and gold has not priced in the hawkish ramifications of resilient inflation.

Likewise, we have noted on numerous occasions that a sharp deceleration in the U.S. labor market is necessary for a dovish pivot. In a nutshell: as long as employment demand outweighs supply, wage and output inflation will remain elevated, and the FFR will need to rise more.

Well, with The Conference Board releasing its Consumer Confidence Index on Dec. 21, the results were hawkish. Lynn Franco, Senior Director of Economic Indicators at The Conference Board, said:

“Consumer confidence bounced back in December, reversing consecutive declines in October and November to reach its highest level since April 2022. The Present Situation and Expectations Indexes improved due to consumers’ more favorable view regarding the economy and jobs. Inflation expectations retreated in December to their lowest level since September 2021, with recent declines in gas prices a major impetus.”

So, while lower oil & gas prices alleviated some of the inflation pressures in November, their drawdowns stemmed from misguided recession fears. Yet, the development spurred consumer confidence and only increases Americans’ ability to spend money on discretionary items.

Please see below:

More importantly, the report stated:

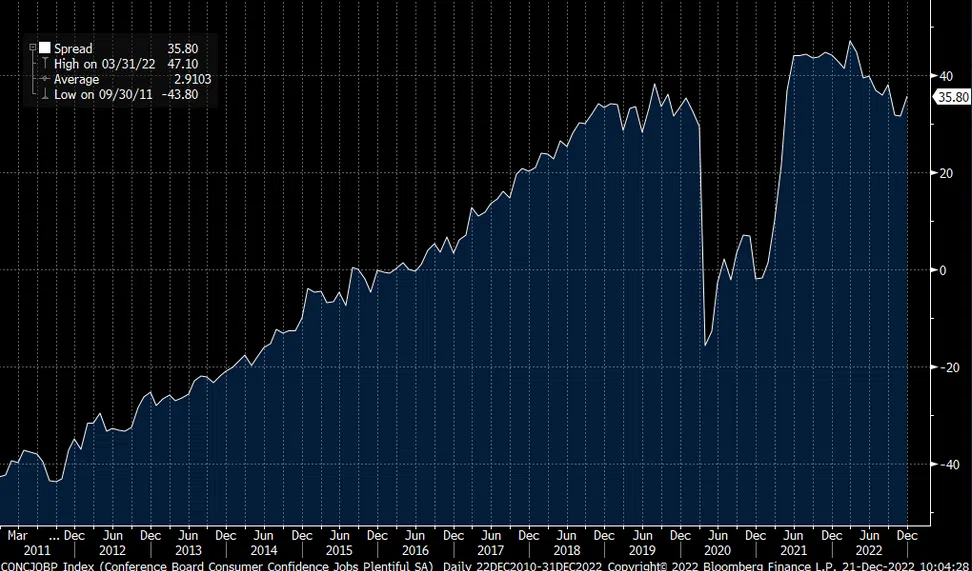

“47.8% of consumers said jobs were ‘plentiful,’ up from 45.2%,” while “12.0% of consumers said jobs were ‘hard to get,’ down from 13.7%.”

Please see below:

To explain, the white line above tracks the spread between jobs are ‘plentiful” and ‘hard to get’ responses. When the white line rises, it means that Americans view the U.S. labor market as more prosperous.

If you analyze the right side of the chart, you can see that the white line has risen recently and remains highly elevated. As such, while job openings have declined slightly and wage inflation accelerated in November, the Fed’s 17 25 basis point rate hikes in 2022 have not created the demand destruction necessary to reduce inflation. Therefore, the FFR needs to rise more than currently expected.

As further evidence, wage inflation is the canary in the coal mine because Americans can afford price increases that much their salary increases; and if wages are running at 5%+, Americans can afford 5%+ output inflation. Consequently, the U.S. labor market imbalance does not support a 2% inflation rate anytime soon.

Please see below:

To explain, the blue line above tracks the average reservation wage expected by Americans in the New York Fed’s latest Labor Market Survey. For context, the metric tracks the lowest average salary respondents will accept for a new job.

If you analyze the trajectory, you can see that the blue line increased from roughly $64,000 in January 2020 to roughly $74,000 in November 2022, which is a 15.6% increase from its pre-pandemic level. Thus, the crowd is uninformed about the economic weakness required to win this battle.

As further evidence, the New York Fed’s survey showed that fewer Americans are searching for work than in July, more are satisfied with their compensation, and expected earnings hit a new series high.

Please see below:

Source: New York Fed

Source: New York Fed

So, with less Americans looking for work and employees expecting higher salaries, the developments are highly inflationary. Furthermore, the fact that these metrics are still diverging despite the FFR’s meteoric rise in 2022 highlights the challenges confronting risk assets in 2022.

Remember, nine of the last 10 inflation fights ended with recessions since 1948; and if inflation was easy to defeat, the historical ramifications wouldn’t be so ominous. In addition, we warned that the FFR has eclipsed the peak YoY core CPI in every inflation fight since 1961. Likewise, since the YoY core CPI peaked (for now) at 6.66% in September 2022, the historically-implied peak FFR is at least 6.67%.

Overall, investors believe inflation will subside with little economic damage, and this misguided optimism uplifts gold, silver and mining stocks. But, a realization requires the Fed to accomplish something it’s only done once since 1948, and as it relates to a lower FFR than the peak YoY core CPI, something it’s never done. Therefore, we’re happy to take the other side of the trade.

Alex Demolitor

Precious Metals Strategist