Ever get confused about the link between inflation, interest rates, and the price of gold? We’ve got you covered.

Let me start by quoting something from the full (premium) version of our today’s analysis:

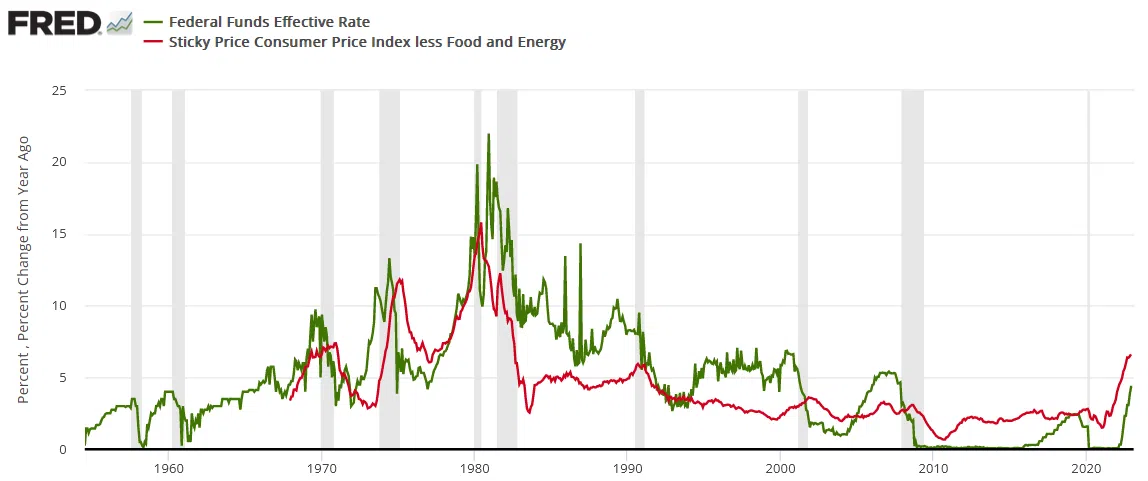

However, we’ve warned on numerous occasions that the Fed has always pushed the U.S. federal funds rate (FFR) above the peak year-over-year (YoY) percentage change in the core Consumer Price Index (CPI), and that nine of the last 10 bouts of rising inflation have ended with recessions.

The latter – likelihood of a recession – means that the stock market (along with silver, mining stocks, and – in particular – junior mining stocks) is likely to fall. Given how far it rose on the various stimulus-based programs, it can also fall substantially. This is not to be taken lightly.

The former implies that either higher rates or lower inflation, or both, are possible. Or at least a faster increase in rates than in inflation (or a slower decline in rates than in inflation).

In fact, let’s see the long-term chart once again.

Here’s what gold did in the long run.

The above chart features the gold price in nominal terms, and the below chart shows the price of gold in real terms (adjusted for inflation based on the official inflation statistics).

Source: Macrotrends.net

The thing that I want to emphasize here is gold’s performance in the 70s and 80s. There were two major declines in gold – one in the mid-70s and another in 1980. Let’s zoom in a bit on the former, as it might not be clear based on the above charts.

Source: chartsrus.com

What happened on the rates vs. CPI chart at those times? There were some major shifts in their relative values.

To make it easier to see what was going on, let’s take a look at yet another chart – the one featuring both nominal and real Treasury yields. Of course, the yields are closely linked to the interest rates, so it’s pretty much the same chart.

The real yield is what is of the greatest importance here.

Why? Because that is what one effectively gets by postponing consumption, saving the capital, and investing (technically, lending) it at very low risk.

If the real yield moves below 0%, it means that one is effectively losing money while just earning interest on Treasuries. That’s when gold becomes highly sought after. Gold pays no interest, but it’s been currency throughout history, so it’s viewed as something safe and stable in the long run. Therefore, it seems better to just hold gold, which at least won’t (theoretically) lose value, while fiat money does. In other words, gold is then used as an inflation hedge.

When the real yields rally, however, the situation turns upside down.

Since gold doesn’t provide interest, and rising real yields mean that it makes more and more sense to have capital in the form of money that pays this increasing interest (like Treasuries), the appeal for gold ownership declines.

That’s why real yields and real interest rates are one of the two key fundamental drivers of gold prices. The other is the USD Index.

Indeed, the lows in real yields (mid-70s and 1980) corresponded to tops in the gold price.

So, again, to clarify:

- Rising real interest rates / yields are extremely likely to trigger declines in the gold price.

- Declining real interest rates / yields are extremely likely to trigger rallies in the gold price.

The above might not work in the short term, but it’s likely to work over the medium- and long term. After all, the markets can be particularly emotional in the short run and move on just about anything, regardless of whether it makes sense or not.

All right, to clarify even more, what exactly are those real interest rates? How to calculate them?

Here’s the definition from Google / Wikipedia.

Nominal interest rate minus the (expected) inflation rate. This approximation will suffice.

Where are the nominal interest rates going now? Higher. Sure, they might be going higher at a slower pace than previously, but they are going higher, and – as history has shown – they will continue to rise until the federal funds rate rises above the year-over-year CPI reading.

The latest year-over-year CPI reading in the U.S. (from Jan. 12, 2023) was 6.5%.

The FFR is about 2% below that.

The above and the historical tendencies imply that either the CPI has to move lower by at least 2% or the FFR has to move higher by 2% while the CPI is unchanged – or some combination of the above (which is most likely).

Either way, this means that the real interest rate is likely to rally by at least 2% from its current levels.

Let me quote what I already stated above:

Rising real interest rates / yields are extremely likely to trigger declines in the gold price.

This means that we are extremely likely to see big declines in the gold price.

What are the real rates doing now?

Well, they are soaring, of course. However, as I wrote earlier, the link between real rates and the gold price doesn’t have to work in the short term, as the markets can focus on all sorts of things due to technical/emotional reasons.

I won’t say that the current rally in real rates is unprecedented, but we haven’t seen this kind of upswing in a long time. The last time, we saw something of at least similar magnitude was right before the year 2000. What happened to the gold price back then?

Gold was after the “Brown Bottom”, but it declined, nonetheless.

In the case of the HUI Index – proxy for gold stocks – it was right before the final part of the slide.

Yes, this is as extremely bearish as it looks.

These are some of the reasons why this short-term rally is a counter-trend rally. The things that I’m covering in my day-to-day analyses are important too, but they are not as important as the above indications. I’m simply not commenting on the things that don’t change that often, but the day-to-day price swings do change often, and I’m commenting on them because they often make people concerned about the outlook.

Speaking of the short-term situation, let’s take a look at what happened and what didn’t happen yesterday.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Thank you.

Sincerely,

Przemysław K. Radomski, CFA

Founder, CEO