As the short-term outlook shifts, more pain could confront the PMs.

While inflation cooled in recent months, as recession fears rocked risk assets in September and October, the pessimism turned to optimism, and the anxiety has reversed. In the process, the PMs have rallied alongside other risk assets, and the developments loosened financial conditions and helped spur more inflation. To explain, we wrote on Dec. 14:

When a hawkish Fed creates recession anxiety, asset prices fall, which helps reduce inflation. In contrast, when a dovish Fed (or the perception of one) reduces recession anxiety, asset prices rally, which spurs more inflation. That’s why we wrote investors’ hopes for a dovish pivot actually reduce the chances of one occurring.

To that point, with the crowd misunderstanding the relationship between financial conditions and inflation, Bank of America warned on Jan. 20 that the pivot narrative should come under pressure in the months ahead.

Please see below:

Source: Markets Insider

Source: Markets Insider

To explain, Bank of America’s Chief Investment Strategist Michael Hartnett told clients on Jan. 20 that China’s reopening will uplift commodity demand and help reverse the energy-driven Consumer Price Index (CPI) decline that materialized recently.

Second, while we’ve warned for many months that a resilient U.S. labor market is bullish for wage inflation, Hartnett noted that rate-cut optimism is premature. He wrote:

While markets are bullishly trading two more quarter-point Fed hikes and 200 basis points of cuts over 18 months, a “super-tight labor market (<200k on initial claims) + renewed rise (in) commodity prices (China reopen + MAD geopolitics in Russia/Ukraine)” could lead to a couple of higher-than-expected CPI prints that reverse investors’ expectations for rate cuts.

As a result, while the crowd misses the link between their optimism and its impact on other markets, the December and January sanguinity should have hawkish implications in the months ahead.

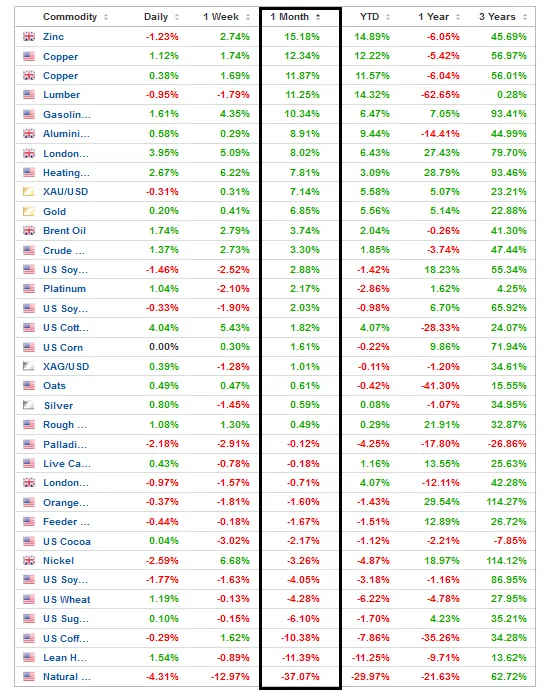

Please see below:

Source: Investing.com

Source: Investing.com

To explain, the black rectangle above shows how several commodities have rallied over the last month, which should put upward pressure on the headline CPI. Furthermore, when China’s reopening gains steam and with Europe escaping the worst of its energy crisis, the outlook for global growth increased; and as economically-sensitive commodities benefit, the backdrop supports a higher peak U.S. federal funds rate (FFR) than what’s priced in.

Please see below:

Source: Cleveland Fed

Source: Cleveland Fed

To explain, the Cleveland Fed expects the headline and core CPIs to increase by 0.53% and 0.46% month-over-month (MoM) in January, which annualize to 6.5% and 5.7% year-over-year (YoY), respectively.

Now, analyzing MoM inflation will be useful going forward, as monthly changes allow for annual estimates of where YoY inflation will go if the current trends persist. Therefore, with these MoM figures well beyond what’s needed for the Fed to reach its 2% mandate, the implications are profoundly hawkish.

To put it in context, 2% annual inflation requires MoM prints of less than 0.17%. So, with the current data tracking well above that, a pivot contrasts fundamental logic. As it stands, while we’ve stated this on numerous occasions, a pivot only occurs if the economic data collapses. But, with that far from the current backdrop, the outlook remains highly bullish for the FRR.

As further evidence, we warned on Dec. 14 that recession anxiety drove energy prices lower and made the short-term inflation outlook bearish. We wrote:

The recent decline in oil prices was driven by investors’ misguided fears of an imminent recession. In a nutshell: if the global economy is on the brink of collapse, demand for oil should suffer mightily.

Please see below:

Source: Google

Source: Google

To explain, the various headlines above depict the recession sentiment confronting the oil market since late September. As you can see, “recession fears” have been making the rounds, and these fears helped reduce oil prices, which helped reduce the headline CPI.

Yet, with that pessimism reversing recently, the commodity comeback is bullish for MoM inflation.

Please see below:

Source: Bloomberg/ZeroHedge

Source: Bloomberg/ZeroHedge

To explain, the red line above tracks the crude oil price, while the blue and black lines above track the wholesale and retail gasoline prices. If you analyze the performances, you can see that all three have declined sharply from their summer peaks, and unsurprisingly, the plunges in December culminated with weak inflation prints.

Conversely, the right side of the chart shows that all three have bounced in January, and China’s reopening should only spur more demand. Consequently, while we’ve warned that inflation does not fall linearly, the more the crowd prices in a pivot, the less likely it is to occur.

Again, a major collapse in GDP growth and employment is the bare minimum for rate cuts; and even the 1970s/1980s showed that the FFR kept rising during three of the four inflation-led recessions. So, with economic growth and employment still resilient and the short-term inflation outlook reversing, our medium-term thesis remains on track.

Please see below:

To explain, the Atlanta Fed updated its Q4 real GDP growth estimate on Jan. 20. The report stated:

“The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2022 remains 3.5 percent on January 20. The nowcast was unchanged after rounding following this morning's report from the National Association of Realtors.

“This is the last GDPNow forecast for the fourth quarter. The first GDPNow forecast for the first quarter of 2023 will be on Friday, January 27.”

Please remember that U.S. real GDP growth was running at ~2% pre-pandemic, and the official data is released on Jan. 26. Therefore, while the crowd has been crying recession and pivot since Q2 2022, the fundamentals have not complied. As a result, the medium-term outlook remains bullish for the FFR, real yields, and the USD Index, and while sentiment has shifted materially, little has changed from a fundamental perspective.

Finally, while the recent data highlights our concerns about jumpy inflation – which means it moves up and down instead of falling linearly – JPMorgan CEO Jamie Dimon said on Jan. 19:

“I actually think rates are probably going to go higher than 5%... because I think there’s a lot of underlying inflation, which won’t go away so quick….

“We’ve had the benefit of China’s slowing down, the benefit of oil prices dropping a little bit,” Dimon said. “I think oil & gas prices probably go up the next 10 years” and “China isn’t going to be deflationary anymore.”

Likewise, Dimon thinks the FFR could hit 6% if only a mild recession unfolds; and not only do his expectations align with ours, but they also align with the historical precedent of where the FFR needs to go to eliminate inflation once and for all.

Source: CNBC

Source: CNBC

Overall, while the pivot narrative persists, cracks are starting to form. With short-term inflation metrics now pointing upward, the December and January optimism has loosened financial conditions and unfolded as expected. As such, with the up-and-down nature of MoM inflation poised to show its might, another bout of panic should hit risk assets over the medium term.

Do you agree with Bank of America’s thesis? And how would the PMs react if rate cuts are priced out of the futures market? Also, why has the economic data held up when everyone keeps predicting an imminent recession?

Alex Demolitor

Precious Metals Strategist